Sterling/Euro Currency Review January 2014

Wednesday 05 February 2014

Last month saw GBP/EUR start the year in much the same fashion as 2013 ended, trading in a tight range with economic data releases very light, says Ben Scott.

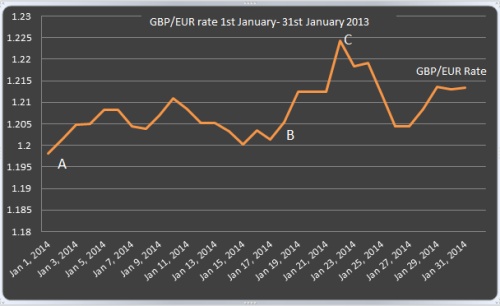

An initial GBP/EUR low of €1.1982 (Interbank throughout) as illustrated by point A on the graph, was followed by a period of gradual increase resulting in a high of €1.2242, (the highest level since January 2013), trading at an average rate of 1.2078 throughout January.

Early January saw the euro struggle for direction, as largely positive economic data lead European Central Bank (ECB) member Nowotny to claim that the outlook for Europe, as a whole, is “much better than a year ago”, yet growing concerns surrounding France, which has the Eurozone’s second largest economy, meant the euro was unable to make any significant gains.

Reports suggest that despite economic improvements in other European countries, the outlook for business and employment in France is at its lowest level for seven months, which combined with the questionable taxation policies of French President Francois Hollande points to further gloom for the euro going forward.

Sterling gains between points A and B remained muted as a combination of lower than expected manufacturing, industrial production and slowing PMI services data fell below expectation, indicating that the UK economic recovery struggled to maintain momentum in Q4 2013.

This could cause concern for euro buyers as evidence grows of a deceleration in economic recovery in the UK, which could result in a decline for GBP/EUR.

Sterling’s gains from point B can be attributed to two very significant factors.

Firstly, retail sale figures in December reached the highest level since 2004, providing a significant boost for hopes of an economic recovery. Sterling’s strength was reaffirmed on the decision of the IMF (International Monetary Fund) to revise UK growth forecast for 2014 from 1.9% to 2.4%, consequently upgrading UK growth forecasts beyond the growth forecasts of UK’s major economic rivals, adding further impetus to the Sterling rally.

The pound enjoyed further strength to point C, touching fresh 12-month highs as it was announced that a job surge during the three months until the end of November resulted in the biggest ever quarterly increase in employment with the rate of unemployment falling from 7.4% to 7.1%.

Although the Bank of England (BoE) have previously admitted that they would consider increasing interest rates when the rate of unemployment falls to 7%, the potential of a rate hike was quickly rejected with the BoE minutes stressing it sees “no immediate need to raise interest rates if unemployment rate hits 7% target”.

Further, Governor Mark Carney reiterated that “Sterling appreciation will hamper export growth”, further reducing the potential of an interest rate increase, which quickly impacted on Sterling. Economists now forecast an interest rate increase by mid-2015 at the earliest.

Outlook

Despite several disappointing economic data releases from the UK providing a shock to a market expecting further economic improvements at the start of the year, Sterling was undoubtedly buoyed by the IMF raising growth forecast for 2014 to 2.4%.

Nevertheless, a simultaneous IMF reduction in the forecast rate of economic growth for 2015 raises some concern; as doubts will again grow regarding the long-term sustainability of the UK economic recovery.

The outlook for the euro going forward remains volatile though. Whilst economic data from Germany including better than expected construction industry sales shows ongoing economic improvements, a recent ZEW report highlights potential concern, with a reported drop in economic expectations and confidence, suggesting trouble may lay ahead for the economic powerhouse of Europe.

Meanwhile comments from derided French President, Francois Hollande, stating that he is looking for public spending cuts of €50billion to fix the French economy could result in further unemployment, economic contraction and social unrest, all of which could lead to further euro weakness.

Elsewhere caution still surrounds ongoing debt talk between Greece and Troika (the IMF, European Commission and European Central Bank) and whilst a repeat of the crisis caused by previous Greek debt concern looks unlikely, tensions undoubtedly remain with Greek Prime Minister Samaras admitting “negotiations with the Troika are difficult”. With Greece recently reversing some of the 2012 mandatory Troika wage cuts, further uncertainty looks probable to the detriment of the euro.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Help with Health Insurance Costs

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.