Sterling/Euro Currency Review April 2014

Tuesday 06 May 2014

April saw Sterling continue edging higher against the resilient euro, despite an unconventional monetary policy from the European Central Bank (ECB) moving ever closer, says Ben Scott.

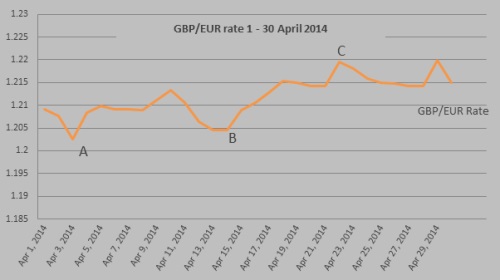

Inconsistent economic data from the UK lead to a disappointing start to the month (illustrated by Point A on the graph) representing the month’s low of 1.2026 and despite edging higher throughout April.

Euro buyers will be concerned by comments from the Bank of England (BOE) warning that a sudden rate rise would “pose a risk to the stability of the market”, making Sterling a far less attractive investment in the short-term.

Currency movements were largely dictated by sentiment and speculation surrounding the Central Bank’s policy. The GBP/EUR pair reached a high of 1.2199 on 29 April 2014, pushing closer to the 15-month high seen in February, trading at an average of 1.2116 throughout April.

Early April saw Bank of England member, Ian McCafferty, continuing previous efforts to downplay the prospect of an increase in UK interest rates stating he has “no expectation of rate rises for some time”.

Sterling weakness was, however, short-lived as a result of comments from ECB President Mario Draghi. Draghi admitted that the ECB “remain[s] unanimous on using unconventional tools if needed” after a significant discussion on the merits of Quantitative Easing (QE). As observed in both the UK and the USA since the onset of the financial crisis, QE in any form would almost certainly prove damaging to the euro.

Sterling gained further support from the International Monetary Fund (IMF), which again raised the UK’s economic growth forecasts from 2.4% to 2.9% for 2014, thereby endorsing UK Chancellor George Osborne’s economic plan, particularly his determination not to abandon austerity.

Nevertheless, disappointing construction data fuelled concerns that the UK’s economic recovery remains consumption driven, led by personal debt, as opposed to a broad-based recovery based on construction and increased exports. If true, this could prove extremely detrimental to the UK’s economy and Sterling in the future. The concern may be well founded given the increase in the UK’s current account deficit, which continues to grow and now stands at approximately 5.5% of GDP.

Sterling gains were re-established from point B; gains which once more can largely be attributed to comments from ECB President, Mario Draghi, who announced, “a further strengthening of the exchange rate would require further monetary policy”.

A strong euro continues to have a double negative impact, firstly, by intensifying disinflationary concerns in the eurozone where inflation has dropped to the lowest level since November 2009; secondly, by reducing demand for exports from the eurozone, which becomes less competitive the stronger the euro is. Exports are crucial for a sustainable economic recovery, making the ECB’s desire for a weaker euro more detectable than ever before.

Despite improving economic data from the eurozone, including better than expected manufacturing and service sector factors from Germany, stabilising unemployment in Spain, and a report from the IMF indicating that Cyprus’s economy is at last showing signs of stabilisation, the euro failed to make any gains.

Sterling experienced a significant boost from the middle of April, on the back of far better than expected unemployment data. Data showed UK unemployment dropped to a five-year low of 6.9% - positive figures which lead markets to price in interest rate increases for the UK as early as Q1 2015.

Outlook

Numerous factors will determine the short term direction of GBP/EUR rates. Whilst the UK’s short-term economic outlook continues to improve, more significant Sterling gains are largely being negated by ongoing concerns of disinflation. This was supported by the announcement that inflation fell to a four-and-a-half year low in April, removing any lingering pressure on the BOE to hike interest rates.

Gains made by Alex Salmond and the Scottish National party in their push for Scottish independence represent the most pressing risk to Sterling. Many major banks are now taking a slightly bearish position on Sterling as concerns surrounding the referendum and the consequential impact on the UK economy weighs heavily on Sterling. We may well see this start to be priced into the market before the referendum in September.

Although economic data is showing signs of improvement in the eurozone, the main concern for the euro remains its actual strength. Bank of France Governor Christian Noyer supports the view that a strong euro is bad for growth and jobs stating, “the stronger the euro is, the more accommodative policy is needed”, endorsing the message of ECB President Mario Draghi, much to the detriment of the euro.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Living Standards in France

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.