Sterling Resilient Despite Bank of England Action

Monday 05 September 2016

August proved to be a relatively flat month for euro buyers as sterling continued to trade within its recent tight range, despite Bank of England intervention to support the economy, writes Ben Scott.

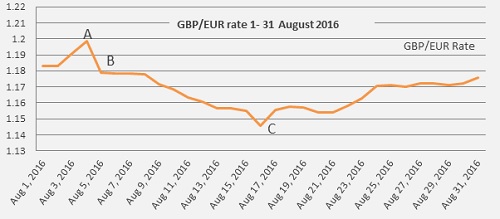

Sterling started the month positively with GBP/EUR reaching a high of 1.1983 August 4th (Interbank throughout) as illustrated by point A on the graph, before slipping lower on the Bank of England’s monetary policy, grinding to a low of 1.1456 on 16th August (point C). GBP/EUR traded at an average rate of 1.1684 throughout August 2016.

Sterling weakness from point A came as the Bank of England announced its first interest rate cut since 2009, cutting interest rates to a record low of just 0.25%. The BoE also took the largely unexpected step of announcing an increase in its monetary stimulus policy, with a further £60 billion of quantitative easing, bringing the total to £435 billion.

Of greater concern, however, was the simultaneous announcement by the BOE of the biggest cut to its growth forecast since records began in 1992, reducing its growth predictions for 2017 from 2.3% to just 0.8%, as economic concerns caused by the UK’s decision to leave the European Union truly started materialise, weighing heavily on the pound.

Sterling weakness from point B came as a result of growing concerns that the doom-filled predictions pre-UK referendum were coming to fruition, emphasised by negative UK manufacturing and construction data, which showed losses in both sectors. This lead to a Reuters poll forecasting that the UK was going to slip into a mild recession with polled economists forecasting economic contraction within the UK in Qtr3 and Qtr4 of 201, with further forecasts suggesting that the BoE would probably cut interest rates further in November 2016 (0.15% to 0.10%).

Sterling continued to fail in its efforts to gain any significant traction against the euro to the middle of the month, point C, where it was boosted by better than anticipated unemployment and retail sales figures, with both beating expectations and largely negating negative economic data from the start of the month.

Sterling was also boosted by higher than expected inflation data which showed a jump in inflation to 0.6% against a forecast of 0.5%. However, it is worth noting that sterling strength on higher inflation figures seems a false move. Higher inflation usually supports a currency as higher inflation usually points to an interest rate hike, which, given the Bank of England’s announcement of monetary stimulus, and the fact that sterling weakness in recent months is a significant contributor to higher inflation, makes an interest rate increase seem extremely unlikely.

Uncertainty and weakness engulfing the pound, particularly against the euro, in August would likely have been far more significant given a positive run of economic data from the eurozone, especially Germany, the key contributor to any economic strength in the eurozone.

However, whilst nowhere near the level of crisis witnessed just 14 months ago, concerns surrounding the debt crisis consuming Greece seem to be growing once again. Faced with an ongoing horrendous economic picture, combined with a broken banking system which is too poor to lend in any attempt to boost economic growth, there is a growing belief that if Brussels (and particularly Germany) fail to soften their implementation of rules, regulations and refusal of debt relief, the best option for Greece might be to leave the EU. Without doubt this would surely throw the euro into turmoil, as seen last year.

Outlook

If economic data in the UK continues to show strength, regardless of the decision to leave the European Union, this would encourage similar votes in other European countries to leave a distrusted and bloated union, adding to cracks which are undoubtedly already growing in the EU’s resolve.

Sterling will unquestionably be buoyed by comments from Germany’s European Affairs Minister, who admitted that the UK will be given special status by the EU, stating the “UK’s size and significance means it will be treated differently”. Yet ongoing economic and political uncertainty is likely to prevent any significant sterling strength given current market conditions - at least until Article 50 is triggered and the UK can start negotiating its exit and future trade agreements. Whilst nowhere near as bad as forecast, the UK’s economic outlook remains unclear.

European economic data has shown improvement in some sectors over the last month. However short-term direction of the euro seems significantly linked to ongoing events in Italy. August saw the euro wobble as another banking crisis was triggered in Italy with the Bank Monti Dei Paschi losing over 16.1% of its value in one day. This before experiencing significant further pressure on the announcement that the bank held €360 billion of non-performing loans leading to fears that the bank could collapse at any time, which would undoubtedly send shockwaves throughout the European banking sector adding significant pressure to the euro.

Additionally, Italian Prime Minister, Matteo Renzi, looks set to heap further pressure on the euro after risking his premiership on a referendum regarding desperately needed institutional reforms in Italy. Whilst Italy is no stranger to changing its Prime Minister, having had four since the financial crisis, this referendum could result in Italy’s long-term membership of the European Union being thrown into doubt. Commentators suggest a ‘no’ vote would be a vote against Brussels and Berlin who the Italian public largely blame for recent harsh austerity and subsequently Italy’s recent economic failings.

If Prime Minister Renzi losses this referendum some analysts have suggested it could be the catalyst for the demise of the European Union and the euro in its current form.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Rental Property Rates Exemption

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.