Sterling Weakness Continues Amid Global Uncertainty

Wednesday 03 February 2016

January proved to be another disappointing month for euro buyers as sterling continued its recent losses against the euro, writes Ben Scott.

Uncertain monetary policy and disappointing economic data in the UK further added to sterling woes last month.

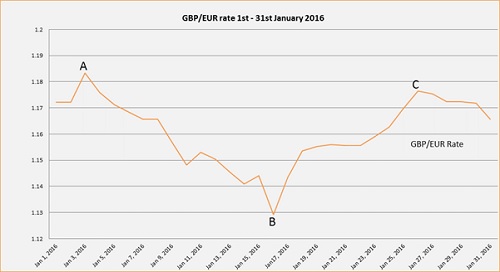

GBP/EUR started the month in reasonable fashion and was able to reach a high of 1.3674 on 5 January (interbank throughout) as illustrated by point A.

With manufacturing and service sector PMI disappointing once more, early in January, and Chancellor George Osborne warned of a “dangerous cocktail of economic risks”. They included tensions in the Middle East, a deceleration in Chinese economic growth, extremely low commodity prices such as oil and copper, reflecting a rapid decline in global economic confidence.

As a result, GBP/EUR traded at a 12-month low of 1.2891 (point C), and an average of just 1.3277 throughout January.

A barrage of economic and political concerns contributed to GBP/EUR losses, notably with oil prices collapsing to 11-year lows, stagnating UK wage growth and the prospect of a ‘Brexit’ (vote to leave the European Union) beckoning, combined with unseasonably warm weather, which resulted in a deterioration of UK industrial production and manufacturing output.

Simultaneously, it is important to note that GBP/EUR losses from point A should largely be attributed to improving economic confidence in the eurozone with the European Central Bank's (ECB) conviction growing that measures previously introduced, including a significant quantitative easing (QE) programme and negative deposit rates, are having a positive economic impact. This was emphasised by Bank of France Governor and ECB member, Francois Villeroy, who stated the “Eurozone economy is picking up”.

Meanwhile, the euro also directly benefited as a safe-haven option against the economic crisis in China, with euro gains throughout January being close to 6% against GBP.

Further, euro gains from point B came on the back of an exclusive Reuter’s article, which claimed many members of the ECB were actually now “sceptical about the need for further (policy) easing”.

This added further credence to the apparent ECB belief that current policy is working, meaning if the ECB does not loosen further monetary policy and that economic growth is indeed starting to get a foothold in the eurozone, then further euro strength remains a credible possibility.

Nevertheless, comments from ECB President, Mario Draghi on 21 January 2016 contradicted this view when he admitted he “expects rates to remain at present or lower levels for an extended period", before emphasising that “downside risks have increased again”.

Draghi went on to provide a clear indication that it will be important for the ECB to review and consider monetary stance in March - the next scheduled ECB meeting - stating, “There are no limits on how far we are prepared to act”. This resulted in the euro giving bank some of its gains after point C on the graph.

Sterling was also boosted at this point on the back of encouraging jobs data growth, which showed the rate of unemployment between September and November fell to 5.1%, representing the best unemployment rate since January 2006.

Outlook

Whilst the Bank of England have admitted that the prospect of a referendum on Europe has weighed heavily on sterling, there remains little doubt that persistently low inflation remains a significant short-term challenge and a concern which continues to weigh heavily on the pound.

The Bank of England admitted in January that it’s own “latest inflation forecast is too optimistic due to falling oil prices”. This again points to an extended period of interest rates remaining at record lows in the UK as a rate hike with inflation so low remains almost impossible, making sterling a far less attractive investment. This was illustrated by HSBC who pushed back its own forecasts of a UK interest rate increase from March 2016 to November 2016.

Whilst UK economic growth for Q4/15 met forecast at 0.5%, there is concern that Britain is continuing to turn into a ‘two-tier’ economy. Whilst the service sector, including retail, banking and tourism, remains reasonably strong, confidence among manufacturing businesses has now fallen below pre-recession levels of 2007. With this sector stagnating, overall confidence for economic growth in 2016 has dipped, again highlighted by HSBC who reduced 2016 the UK growth forecast from 2.4% to 2.2%.

Whilst European economic data has shown improvements recently, Europe faces a year of extreme economic, political, social and geopolitical risk over the coming 12 months, which could easily prove detrimental to the euro.

All in all, 2016 has started in a well and truly tempestuous fashion, and there are some signs of recovery in the property market in France, notably in the large increase in sales last year.

With this in mind we anticipate that A Place in the Sun Live international property exhibition at Manchester will be busy, and many prospective buyers will be focusing on forward contracts for their currency requirements. We looking forward to meeting you in the French Village at the exhibition.

To find out more about how a forward contract can help you in the current market, you can also contact Ben Scott at FC Exchange on the link below.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Air France Struggles with Transavia

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.