Does Voluntary Health Insurance in France Make Sense?

Tuesday 03 June 2008

Does it make sense to take out voluntary ('top-up') health insurance in France, or pay as you go?

With Sterling plummeting against Euro past year, with food and energy prices going through the roof, many expats are looking around for ways of making economies in their household budget.

From the e-mails we have received on the subject of French health insurance, some our readers in France seem to have decided to adjust their health insurance expenditure, either cancelling their voluntary health insurance policy, or considering doing so.

So, does it make sense to cancel your voluntary health insurance policy, or are there alternatives available in France?

Let us just recap on the basics. Whether you are retired, or you run your own business in France, the French social security system reimburses only a proportion of your French health charges.

As a general rule, you will receive about 70% level of reimbursement (80% for hospital treatment), with the balance either having to be paid by you as you go, or from a voluntary (top-up) health insurance policy.

According to the magazine Panorama de l’assurance santé, between 1995 and 2005 the cost of these policies doubled.

A couple in their early 60s could now expect to pay between €1000 - €2500 a year for a French voluntary health insurance policy, with policies at the bottom end offering a minimum level of complementary cover, whilst others will reimburse almost all your health costs.

On this basis, therefore, if you were only using the French health service for occasional minor ailments, it is unlikely that it would be worthwhile to take out voluntary health insurance in France.

Nevertheless, we do not take out house insurance merely to cover the possibility that a glazing pane will be broken in a storm; we do so against the risk that the roof may be blown off the house.

The same principle applies to voluntary health insurance in France, except that the comparison cannot be take too far.

This is because, if you incur a ‘major illness’ in France, the costs of French health care are covered by the social security system.

To a large extent, therefore, your voluntary health premiums are being paid to reimburse minor charges, incurred for consultations with your doctor and the medicines you are prescribed.

This might lead to a conclusion that, for many people, it would be cheaper to 'pay-as-you-go'. However, let us not be too hasty, for the picture is complex, and one that is in a process of change. You need to consider a number of factors:

- The definition of what constitutes a 'major illness’ is strictly defined, and any treatment you receive in a hospital beyond the list of prescribed illnesses will only be covered at the rate of 80% of the official rate.

- Even though you may be eligible for 100% reimbursement because of a major illness, the majority of consultants now impose charges over and above the official rates, which are not reimbursed by the French social security system.

- There are also other hospital costs that are not covered by the French social security system. These include a daily charge of €16 for a stay in excess of 24 hours, a charge of €18 for treatment in excess of €91, the extra cost of a private room, and charges for a telephone and television.

- As we reported in a recent newsletter, the French Government has stated it intends that voluntary insurers should pick up a larger share of the health costs, with the prospect that the list of those charges that will need to be met by the voluntary insurers, or patients, will increase.

- Finally, and most importantly, there is a need to consider your age and medical circumstances. Most expats who relocate to France are aged 50+, with medical needs that are likely to reflect this level of seniority.

Accordingly, it is by no means self-evident that cancelling your top-up health policy makes economic sense. Aside from the cost, you also need to consider the psychological benefits of having voluntary health insurance cover, giving you the peace of mind you may need to enjoy your life in France.

Nevertheless, if you are prepared to pick up routine medical treatment in France yourself, you might find it more economic to take out a ‘hospitalisation’ plan.

These policies are not widely advertised by the voluntary insurers, nor are they offered by all of them, probably because they are not as lucrative as the more general policies.

In a recent survey, a French consumer magazine found that 'hospitalisation only' policies were up to 80% cheaper than a basic general policy.

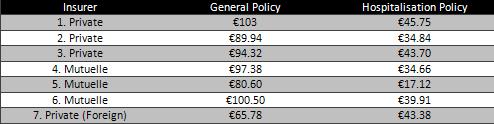

The following table shows the monthly rates offered, for a couple in their early 60s, by seven private and mutuelle insurers on a general policy, and those for a 'hospitalisation only' policy.

Voluntary Health Insurance Premiums

Source: Le Particulier

In considering the choice of a 'hospitalisation only' policy, the key criteria you need to focus on are the level of reimbursement of the daily charge (frais de séjour) and of the excess consultants’ charges (dépassements). The French social security system will reimburse only at the basic rate, whereas actual rates may be 200% to 400% of this rate.

Thus, whilst the Policy number 5 offered the lowest rate for a hospitalisation policy, it only offered reimbursement of hospital costs at the official rate, and the rates offered for a private room were also the lowest. The other policies offered up to 400% of the official rate.

To find a suitable policy, you could do a lot worse than consulting some sites that offer comparative rates between different insurers:

Alternatively, enter assurance complémentaire santé in your search engine and seek a quotation from one of the insurers you will find listed.

As an alternative to reducing your insurance cover, you may also wish to consider making application for assistance towards your insurance costs.

Under a scheme called chèque santé a couple over 60 with a net taxable income of less than €13,000 per year would be eligible to receive a contribution from the social security system of €400 towards their policy. You can read more at Assistance with Voluntary Insurance Costs.

We would be interested to know more of your own experiences, either on our Forum, or e-mail [email protected]

Have you yet read our free, comprehensive and authoritative guide to French Health care?

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.