Sterling/Euro Exchange Rate Review Jan 2019

Thursday 07 February 2019

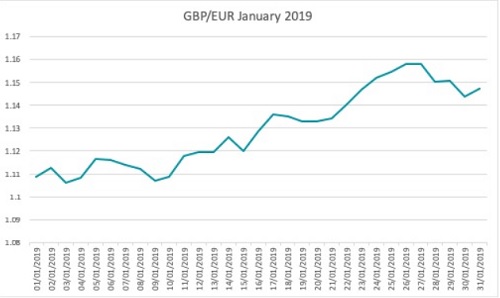

The Pound to Euro exchange rate began 2019 at €1.11, before recovering to 20-month highs above the key €1.15 resistance barrier, writes Ben Scott of Global Reach.

The start of the year has already been action-packed for the markets. A flash crash at the beginning of January and a number of political developments have kept investors alert, as they try to predict what will happen next.

UK service sector slows, and inflation cools

At the beginning of January UK service sector data was released for December, which showed subdued growth. The ecostat is of high importance for markets as it’s the largest indicator for British economic activity.

Business confidence in the sector reached its second-weakest levels since the Global Financial Crisis, with Brexit named as the cause. Meanwhile, job creation in the service sector faltered to a 29-month low.

Accompanied by the manufacturing and construction sector prints, January created more concerns that perhaps UK growth would be heading towards a standstill in the last quarter of the year.

Another ecostat investors were watching for was the Consumer Price Index (CPI). Inflation reached a 20-month low in November, hitting 2.3% after crude oil prices fell.

By January 11th, the Pound had risen against the Euro as the prospect of postponing the UK’s exit circulated.

On the 17th January, the Pound was offered some further support when Theresa May survived a vote of no confidence in the government.

On 25th January there was another surge higher for Sterling against the Euro when the European Central Bank (ECB) pressured the common currency lower with a cautious tone and commented that economic growth would be weaker than expected.

Eurozone data raises concerns about recession

The Eurozone hasn’t had the best start to 2019, with economic data showing Italy dipped into recession, and German growth concerns played on the minds of many. Gross Domestic Product (GDP) figures showed a decline of -0.2% in the last three months of the year, after a -0.1% contraction in the previous quarter. The Eurozone as a whole grew by only 0.2% in the fourth quarter of 2018, the joint-weakest expansion in four years.

Bank of England awaiting Brexit decisions

It seems as if BoE policymakers are at the ready for any signs of Brexit developments.

January saw BoE Governor Mark Carney state that policymakers will be ‘prudent not passive’ after the UK leaves the EU. Carney also suggested that the Pound’s value could be damaged if more signs of weakness between the EU and UK’s relationship appeared. Carney said: ‘The nature of that partnership is currently the subject of feverish debate in parliament, and the prospects for Sterling will depend heavily on how Brexit actually progresses… From a monetary policy perspective, the Monetary Policy Committee is well-prepared for whichever path the economy takes. We have the tools we need. We will be prudent not passive.’

Brexit has been the primary source of Sterling movement in January, given that Theresa May suffered a historic defeat in parliament on her Brexit deal.

However, despite a lot of voting and political uncertainty, Sterling remained quite buoyant in the market. Towards the end of January, the Pound to US Dollar (GBP/USD) exchange rate breached 1.31, stepping beyond the 1.30 key psychological barrier to a three-month high, while creeping above the 1.15 threshold against the Euro to reach a 20-month pinnacle.

GBP/EUR Forecast

Data at the start of February has shown the UK services sector slowed in January, almost to a standstill.

Markit’s Services Purchasing Managers’ Index (PMI) sank to 50.1, barely above the 50.0 threshold which separates expansion from contraction.

Construction and manufacturing data has also been lacklustre, signalling growth in the first quarter could be disappointing. UK car sales have also dipped in January as economic anxiety sweeps Britain off the back of Brexit fears.

Meanwhile, growth in the Eurozone will be another factor to watch closely; with France and Italy posting particularly weak numbers, there could be more struggles ahead which could weigh on the Euro exchange rate. Germany’s apparent slowdown could be another major influencer on the common currency. The upcoming European elections will be another event to watch with the potential for populist parties to gain some favour.

Brexit is likely to be the key driver for Sterling moving forward, and so the outcome of months of political discussion will be one to watch as Britain nears the 29th March Brexit day. In the event the UK chooses not to leave the EU, both the Pound and the Euro could be supported.

Ben Scott

Global Reach

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.