Sterling/Euro Exchange Rate Review April 2018

Tuesday 08 May 2018

April was a mixed month for sterling, which experienced some big swings against the euro, as markets tried to decide whether the Bank of England would raise interest rates, writes Ben Scott of FC Exchange.

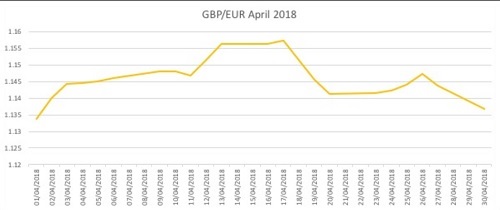

The pound to euro exchange rate came full circle in April, beginning the month at interbank levels of €1.13 and closing the month at the same level.

However, the points in-between saw sterling flirt with €1.16 on 17th April, before dropping in the latter part of the month to achieve six-week lows on April 30th.

Sterling softness was even more dramatic against the US dollar (GBP/USD), which ebbed away from highs of €1.43 seen in the middle of the month, to €1.37 by the close of April.

At its peak, April saw GBP/USD reach its highest level since the Brexit referendum.

Bank of England Speculation

The rise and fall of the GBP/EUR exchange rate was predominantly down to speculation on whether the UK could soon see higher borrowing costs. UK data was positive and investor sentiment was buoyed.

The UK’s unemployment rate recorded a fresh 42-year low at 4.2% in the three months through February on the year, and wages finally managed to overtake inflation. Average weekly earnings came in at 2.8% in the same time period, while including bonuses the figure held steady at 2.8% from the previous month.

The data seemed to indicate that the economy was tightening, and investors hoped this would give further momentum to the motives of Bank of England policymakers and add to the pound’s rally.

Nevertheless, on the 18th April the pound dropped against other currency majors as UK inflation missed forecasts entirely. Consumer prices dropped to a one-year low in March and hopes for a UK interest rate hike began to falter. Institute of Directors senior economist Tej Parikh commented: ‘Today’s figures show a significant drop in inflation, and it is expected to continue to fall over the course of this year. This will be welcomed by the business community who have seen high inflation act as a major speed bump on economic growth ever since the beginning of last year.’

Super Mario

The euro had central bank problems of its own in April. Dovish comments from the European Central Bank (ECB) pressured the single currency lower as markets priced in looser monetary policy for a longer period.

On the 26th April the pound began to climb against the euro again following comments from European Central Bank President Mario Draghi. The latest central bank statement said that the asset purchase programme would remain in place until September, at the very least, while iterating that interest rates would be unlikely to move for some time after it ends its quantitative easing push.

Draghi also acknowledged the recent blip in economic data and speculation that the Eurozone was undergoing a slowdown, stating that policymakers were ‘cautious’ about the recent hit-and-miss data regarding the first four months of the year. He stated: ‘Don’t get me wrong, we are concerned about these developments. It’s not like we take this all with indifference.’

Forecast

Things took another interesting turn at the start of May, with Eurozone inflation slipping below forecasts, coming in at 0.7% in April down from 1.0% the previous month.

With data like this the ECB has less reason to take its foot off the gas when it comes to their accommodating monetary policy stance. This would mean quantitative easing could go on for longer, and interest rates could remain lower for some time.

Brexit developments could create some GBP/EUR movement as the UK government fights over whether to remain in a customs union, and the next Brexit summit in June approaches.

At the start of May Theresa May stumbled when her inner cabinet voted against her customs union deal proposal, six to five. One of the votes that tipped the scale came from newly appointed pro-Brexit Home Secretary Sajid Javid, just three days into his new role. Her leadership has once again come into question, meaning that the face of UK politics could be rocky once more, especially if any more resignations take place.

Other factors investors will be watching for is growth numbers. While the Eurozone is still producing better growth numbers than the UK, markets will be watching for more solid signs of a slowdown. The UK’s growth numbers will be particularly sensitive given the recent 0.1% GDP revelation. A slip lower could be bad news for Sterling which could sink even further.

If UK inflation continues to decline there’s little argument for the Bank of England (BoE) to begin raising interest rates, especially when considering the recent economic data. The possibility of an increase has been a significant influence for sterling in recent months and so any developments or speculation regarding the central bank and monetary policy could also influence the pound.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.