Why Does the Euro Remain so strong?

Thursday 04 October 2012

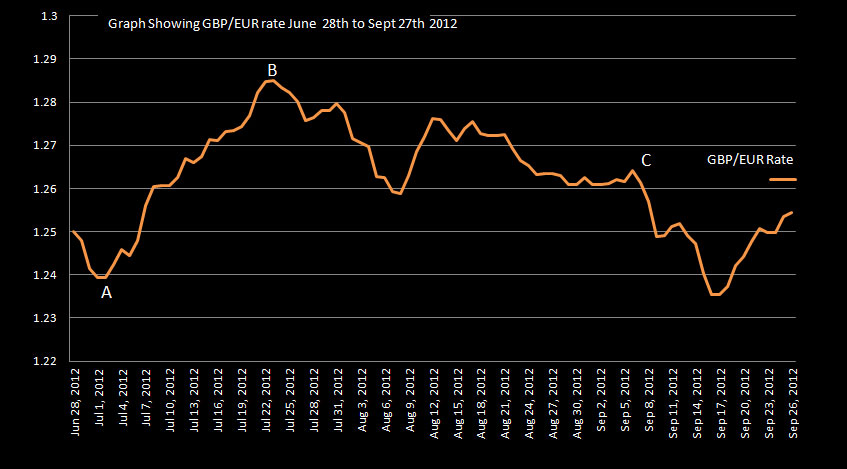

Sterling traded positively against the euro at the start of the third quarter, but later lost ground due to deteriorating economic conditions in the UK, writes Ben Scott of FC Exchange.

Sterling touched a 44-month high of 1.2851(interbank) in July before a low of 1.2354 in September, trading at an average of 1.2623 during Q3 2012.

Despite positive moves for Sterling, the euro’s ability to strengthen so aggressively in spite of the ongoing debt crisis continues to cause concern for euro buyers, as illustrated on the graph below.

Sterling gains against the euro (from point A on the graph) saw Sterling peak at 1.2851 on 23rd July, the highest rate since November 2008, but hide the fundamental weakness of the UK economy; a weakness in the manufacturing, construction and services sectors, resulting in the pound losing ground against most major currencies. The consequential threat of further quantitative easing (QE) weighed heavily on Sterling, but gains against the euro, from point A, once more emphasise the crisis engulfing the eurozone.

The European debt crisis was again the driving factor of euro weakness as concerns that the European Union (EU) and European Central Bank (ECB) had failed to deal with the ongoing debt crisis. Threat of debt contagion once more gripped the markets throughout Q3, a point emphasised by the cost for Spain to borrow money continually breaching 7% - the level at which countries such as Greece, Ireland and Portugal were forced to accept a bailout.

Statements from German Finance Minister, Wolfgang Schaeuble, claiming that the “mere perception of insolvency risk in Spain could cause contagion in the eurozone”, demonstrates how substantial a threat the Spanish crisis had become to the euro.

Euro weakness was compounded between points A and B as confidence declined in the countless rescue plans proposed to save the euro, all of which had failed to result in a resolution, whilst the suggestion of 'Euro Bonds', which ECB member Knott stated would be “needed in the end”, were initially rejected by German Chancellor Angela Merkel, despite the backing of most European members, thereby highlighting the political division which weighed so heavily on the euro.

The decision by the Bank of England (BOE) to inject a further £50 billion of quantitative easing into the UK economy failed to cool Sterling’s gains against the euro in early July, as the ECB immediately cut interest rates from 1% to 0.75%.

Meanwhile, ECB President Mario Draghi’s comment on to “expect a slow recovery” went some way to validating concerns that the action of the EU and ECB were insufficient in dealing with the economic crisis.

The Bank of England’s introduction of the FLS (Funding for lending scheme), aimed to inject liquidity into the banking system, whilst announcing a new £80 billion lending programme went some way to justify Sterling’s superiority against the euro in mid-July as continued political division between core and peripheral European countries weaken the euro.

Speculation that Greece, once more, needed to renegotiate the terms of its bailout or be forced to leave the euro, and the request from Valencia for help from the Spanish central government to make the regions debt repayment on its behalf, were the driving factors which saw the euro value plummet immediately before point B on the graph.

Euro Strengthens Against Sterling

The pound’s decline against the beleaguered single currency, following point B, was instigated by a far larger than expected drop in gross domestic production (GDP) for the UK (Q2 2012). Expectations were for a -0.2% in economic output during this period, but the official figure showing a drop of -0.7% (the largest drop in economic output for 3 years), sent shockwaves through the markets, confirming the UK economy was in its first double-dip recession since the 1970s.

These losses would have been even more substantial were it not for the growing concerns that Spain would be forced to seek a full-blown bailout shortly after receiving clearance on a €100 billion banking bailout.

Simultaneously, the deteriorating economic outlook in Germany lead to credit rating agency, Moody's, putting its vital AAA credit rating on negative outlook (the first step towards a negative downgrade), emphasising concerns that "Germany was at risk from the increased likelihood of a Greek exit from the euro and the need to provide more [financial] support to Spain". Any negative downgrade for Germany, the key economic contributor of the eurozone would prove disastrous for the euro.

Euro gains against the British pound towards the end of July resulted from ECB President Mario Draghi’s declaration pledging unconditional support for the euro, stating the ECB was "ready to do whatever it takes to preserve the euro, believe me it will be enough". This afforded vast support for the euro and finally provided the markets with a belief that the euro crisis could and would be resolved.

This positivity, however, was very nearly reversed as Mario Draghi's comments following the ECB rate decision (02.08.2012) left the markets contemplating another case of 'over promising and under delivering' as the ECB failed to commit to a bond buying programme.

Uncharacteristically, on 8th August Bank of England Governor, Mervyn King, provided some much needed respite for Sterling by declaring that, "further cuts to the bank base rate would prove detrimental to some UK institutions", indicating interest rate cuts were unlikely in the short-term. So doing, rejecting recommendations from IMF chief Christine Lagarde that a cut from 0.5% would be required to stimulate the faltering UK economy.

Euro firmly re-established strength towards the end of August, despite speculation that Greece would request extensions to implement austerity measures, and the admission from the Mayor of Madrid that "a Spanish bailout seems inevitable".

Further improving euro sentiment were the rumours that Chancellor Angela Merkel was backing the ECB President’s plans to reduce the inflated cost of borrowing money for struggling peripheral European countries - a major cause of euro instability over the last few years. Added to this, comments from Angela Merkel that holding the euro together is "worth every hardship and effort" provided much needed euro unity going into September.

From point C on the graph, euro strength came, initially, as the ECB and Mario Draghi finally announced their revolutionary, unlimited sterilised bond buying programme, which had been hinted at throughout Q3 2012.

Despite being leaked to the press, the programme dubbed OMT (Outright Monetary Transaction) was received with elation as the ECB finally announced a credible plan which would aid struggling countries such as Spain and Italy, and potentially rescue the 16- nation single currency.

Additionally, despite some late opposition, Germany's highest courts finally backed the establishment of the ESM, establishing a £400 billion eurozone bailout fund to run alongside the OMT. Chancellor Angela Merkel claimed "Germany was sending a strong signal to Europe, the first step to resolve the euro crisis has been taken".

Another significant catalyst for euro strength came on 13th September, a result of US Dollar weakness as opposed to euro strength. With EUR/USD being the highest traded currency pair, any US$ weakness usually results in euro strength and this was the case when the Federal Reserve announced a new round of its asset purchasing programme (QE3). As anticipated, this announcement resulted in dollar weakness which saw the euro strengthen, particularly against Sterling.

Sterling weakness was intensified by forecasts that the UK would fail to move out of recession for the rest of 2012, whilst growth forecasts for 2013 were also significantly reduced.

Outlook

Going forward, several key factors will determine the direction of GBP/EUR exchange rates in the short to medium term.

Data from the UK continues to suggest Chancellor George Osborne’s austerity plans are failing to work and whilst the UK clings on to its vital AAA credit rating, concerns are growing that a credit cut is moving ever closer an ongoing double-dip recession, with negativity for Sterling expected as a result.

Economic figures in the UK continue to disappoint with BOE Governor, Sir Mervyn King, admitting that "output has barely grown in a year and a half", whilst forecasts predict growth of just 1.5% for all of 2013 - Sterling strength looking unlikely without sustainable economic growth.

Although the announcement of the OMT from the ECB and Germany giving the go ahead to the eagerly awaited ESM (European Stability Mechanism) created short-term relief for the euro, ECB President Mario Draghi was very clear in spelling out that the ECB has merely brought time for the European political leaders to implement the structural reforms required to lead Europe out of its economic crisis. Markets will watch closely to determine if politicians are successful in implementing necessary reform, but as stated by the Dutch Prime Minister, "although progress has been made in Europe; it's too soon to say the worst is over".

As has been all too obvious in recent years agreement between European politicians is all too hard to come by and the lack of harmony amongst the political elite is definitely the biggest obstacle to euro strength in the future.

Comments from one of the original founders of the euro, Otmar Issing, claiming that “Everything indicates the euro will survive, but how many countries will be able to be a part of it in the long term remains to be seen”, points to further volatility for the euro.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.