Sterling/Euro Currency Review Q4/10

Tuesday 18 January 2011

Sterling experienced a mixed performance against the Euro for the majority of the final quarter of 2010, writes Ben Scott.

A blend of economic data and sentiment prevented any sustainable movement for either currency.

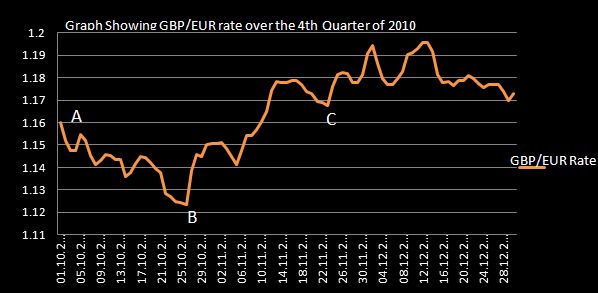

Sterling saw a high of 1.1997 (interbank) against the Euro and a low of 1.1180 (interbank) in the period of as the pair failed to hold onto any short-term gains.

Despite the average GBP/EUR exchange rate dropping from 1.2019 (interbank) in Q3 of 2010 to 1.1636 for Q4, it is the unpredictable outlook for 2011 which will be causing concern.

Broadly speaking, the average GBP/EUR rate seen in Q4 dropped by nearly 4 cents compared to the average rate seen in Q3 2010.

The decline of Sterling’s fortune against the Euro throughout October was particularly surprising as the UK finally seemed to have fought off the threat of a double dip recession towards the end of Q3, lead by a substantial increase in Britain’s construction sector at the end of September.

However between points A and B on the graph, Sterling weakness can be attributed to many economic factors, such as falling house prices (which dropped 3.6% in September alone) and slowing confidence in the UK economic recovery. Manufacturing and production forecasts, vital for the UK economic recovery, fell significantly in anticipation of the Government’s austerity measures announced on October 20th, causing a sustained negative effect on Sterling in this period.

Euro Strenghtens

Concurrently the Euro was strengthening on the back of significant economic and industrial production data particularly from Germany. At this point Germany maintained its position as the largest and most economically important state in the Euro-zone and its sustainability was seen to underpin the Euro despite the economic picture in a majority of the Euro member countries deteriorating at the same time.

In this period the Euro was also the main beneficiary of a so called ‘Currency-war’ (competitive devaluation of a country’s currency) between the US and China in a bid to increase their export competitiveness. Therefore, the Euro was seen as the main benefactor, as investors removed holdings in the US$ and the Euro strengthened in its capacity as the only viable alternative to the US$.

The Euro also made gains in this period as the substantial fiscal bailout of Greece subdued the threat of default from any European country. In essence the worry remained, but to a lesser extent, about Spain, Portugal and Ireland defaulting on their debts.

In the period just before point B on the graph Sterling reached its lowest trading point since March 2010, after announcements that the UK’s net borrowing for September hit a staggering £15.6 billion, the highest monthly borrowing level since records began in 1993. Debt in the UK is a huge concern, and looks set to continue dictating Sterling’s direction throughout 2011.

Despite the announcement on October 20th of £80 billion of spending cuts in the governments ‘Comprehensive Spending Review’, the original perception was positive as Credit Rating Agencies endorsed the measure by saying such actions would preserve the UK’s much revered AAA credit rating, as debt was being reduced.

Concerns About Quantitative Easing

Concerns were however growing about imminent Quantitative Easing (QE) on top of the £200 billion already injected into the UK economy, which weighed heavily on Sterling. Bank of England Monetary Policy committee members Adam Posen and David Miles, British Chamber of Commerce chief economist David Kern and Chancellor George Osborne all seemingly added their support to further QE with Chancellor Osborne saying he would support monetary stimulus, “should the Bank of England deem it necessary”. This all contributed to Sterling weakness, as Quantitative Easing will always have a negative effect on a currency where implemented.

The sharp rise immediately after point B on the graph is a direct result of better than expected economic growth figures in the UK for Q3, (Gross Domestic Production (GDP) for Q3 came in at 2.8% against estimates of 2.4%).

Irish Bailout

However the almost continuous rally for Sterling thereafter until point C on the graph is a result of Euro weakness, as concerns surrounding the ability of Greece, Portugal Spain and Ireland to reign in their debts intensified, ultimately leading to the financial bailout of Ireland (officially announced on 28th November but known days in advance) costing up to £85 billion. This lead to mass demonstrations and riots in Ireland, as it appeared Ireland's best interest had been sacrificed by the European Union for the greater good, in particular protecting the Spanish financial system from collapsing, as Spain is seen as too big an economy to fail. In short, previously quelled fears had been reignited.

Despite Sterling’s attempts to break above 1.20 (interbank) on several occasions in the aftermath of the Irish Bailout (point C on the graph), and looming sovereign risk issues throughout Europe that followed, the 1.20 (interbank) level was not breached.

Sterling’s failure at the 1.20 barrier was largely due to the fact that the UK had seen it necessary to contribute approximately £7.5billion directly to the Irish bailout, despite the UK’s own austerity measures.

This meant any potential Sterling strength was negated by concerns surrounding UK exposure to Irish debt. Prime Minster David Cameron said of this exposure the UK must play its part due to the “incredibly close economic relationship (between the UK and Ireland) and that “we export more to Ireland than we do to Brazil, Russia, India and China combined”.

Consequently despite claims from UK Foreign Secretary William Hague that the “single currency might not survive”, the UK’s exposure to Irish debt, the continual threat to a key consumer of the UK export industry, and an overall deteriorating economic outlook in the UK meant Sterling was unable to benefit from the Euro instability at this time meaning the Sterling-Euro rate remaining relatively flat throughout December.

Outlook

Going forward numerous factors will dictate the direction of GBP/EUR exchange rate with the economic outlook for both the UK and the Euro zone still struggling to establish any form of meaningful recovery, making pin-point accurate forecasts impossible.

Importantly, Sterling’s short term aspirations are threatened by inflationary pressures. UK inflation expectations for 2011 currently sit at 3.5% and significantly higher than the Bank of England inflationary target of 2%, which could lead to interest rate increases.

Although a currency would usually strengthen on the back of interest rate hikes, interest rate increases at a time where unemployment is likely to continue rising, when house prices and mortgage lending figures are deteriorating, and the overall UK economy is still threatened by a double dip recession higher interest rates, could be extremely detrimental to the medium term strength of Sterling.

As former bank of England member David Blanchflower recently stated, “It would be George Osborne’s worst nightmare if the UK Central bank began raising its interest rate this year”.

On the other hand, concerns remain regarding the ability of many European countries to implement appropriate fiscal policy to deal with their growing debt burden. After the financial bailouts of Greece in the middle of 2010 and of Ireland at the end of November the fear is that speculative traders will target other European countries in 2011 who are apparently struggling with their debt obligations. Many commentators are watching Portugal now and keeping a close eye on Spain.

The single currency seems set to continue to struggle with recent surveys showing 48% of Germans want an immediate return to the Deutsche Mark.

However, Sterling is hardly in a position to capitalise as concerns surround, the weakening UK economy, spiralling inflation and the threat higher interest rates could have in a depressed economy. There are indications that sterling could enjoy a short term push higher.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.