Sterling/Euro Currency Review Q3/10

Friday 15 October 2010

Sterling performed steadily against the Euro for the majority of the third quarter before significant negative pressure finally forced it lower, writes Ben Scott.

The result was that it gave back all of the positive gains made in the second quarter.

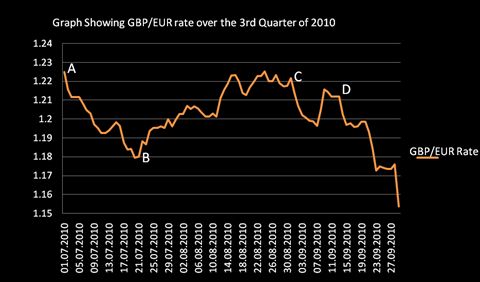

Sterling slipped from a high of 1.2391 (Interbank) on the last trading day of June to a low of 1.1565 (Interbank) at the end of September, representing the lowest trading level for GBP/EUR since April 2010.

Despite the average GBP/EUR exchange rate improving from 1.1706 (Interbank) in Q2 to 1.2019 (Interbank) for Q3, it is the significant losses experienced towards the end of September that will cause great concern for Euro buyers, as illustrated on the graph below.

Broadly speaking the GBP/EURO rate dropped by over 8 cent throughout Q3, compared to a gain of 4 cents in Q2.

The decline in Sterling’s fortunes against the Euro over this period can be attributed partly to the deteriorating economic outlook in the UK, prompting concerns that the UK could slip into a dreaded double dip recession.

More significantly, Sterling’s loses can be linked to considerable improvements in the perceived economic recovery of the Euro Zone.

This is despite numerous European countries experiencing severe financial pressures and credit rating downgrades as a result of their inability to deal with spiralling debt issues.

The point was emphasised as recently as 30th September when Spain had its credit rating cut from its coveted AAA credit rating to Aa1, by Credit rating agency Moody’s. Throughout Q3 the Euro-Zone has been hit by growing concerns that Portugal, Ireland and Spain were all set to experience financial meltdown comparable to that experienced by Greece earlier this year.

However, concerns regarding the UK's ability to sustain an economic recovery as good as that being seen by Europe reached crisis point at the start of September (point C on the above graph) when the European Central Bank took the unexpected step of raising growth targets for the Euro Zone from 1% to 1.6% for 2010, whilst UK growth forecasts were diminishing.

Threat of Quantitative Easing

There is also the constantly growing threat that the Bank of England will be forced to introduce further ‘Quantitative Easing’ (QE), on top of the £200 billion pounds previously injected into the economy since the onset of the economic crisis in August 2007.

This has weighed heavily on Sterling in recent weeks and looks set to continue pushing Sterling lower in the short term, a point supported by the graph above.

The sharp drop immediately after point A on the graph indicates the start of the decline for Sterling after the UK experienced an improvement in its financial sentiment towards the end of Q2.

This followed announcements from the newly formed Conservative-Liberal coalition government that improving the financial situation and cutting the budget deficit in the UK seemed to remove the threat of a possible downgrading of the UK’s revered AAA credit rating.

Sterling’s weakness between points A and B indicate just how significant a threat QE is to a country's currency performance, (and this continues to pose a significant threat to Sterling going forward).

During this period economic output and sentiment dropped in the UK leading to calls for further QE to stimulate a faltering economic recovery, and this subsequently lead to Sterling weakness.

The start of the significant and sustained push lower for Sterling/Euro rates from 7th September (Point D on the graph) until the end of September came as a result of continuing speculation surrounding concerns that further QE is to be announced imminently in the UK.

The massive dips towards the middle and end of September can be more accurately attributed to the Euro being seen as the only real alternative to the US$, which is also weakening significantly.

Outlook

Going forward numerous factors will dictate the direction of GBP/EUR exchange rates in the months leading up to Christmas with the economic outlook for both the UK and the Euro zone deteriorating towards the end of Q3, making meaningful forecasts impossible to make.

Contradictory comments from senior Bank of England Monetary Policy Committee members Andrew Sentence and Adam Posen at the end of September contributed to negative Sterling sentiment.

Andrew Sentence appears to be a lone voice in calling for higher interest rates and a halt in Quantitative Easing. Most Financial experts expect Adam Posen to be supported in his encouragement for further QE after stating: ‘'More is needed to be done to stimulate the economy”, before adding that failure to act could “undermine our long run of stability and prosperity.'’

Although it is still impossible to evaluate the overall effect of QE in the long term, the process of artificially injecting money will almost certainly have a detrimental short term affect on Sterling, as seen throughout earlier implementations of this policy.

When combined with falling factory output figures, dropping levels of economic confidence, and the banks ongoing stubborn refusal to increase lending, this uncertainty has seen the UK public continue their cautious financial approach.

So with further hard hitting and wide reaching budget cuts set to be announced on October 20th by Chancellor George Osborne, Sterling’s weakness looks set to be extended further throughout Q4.

Euro Zone Doubts

On the other hand concerns remain regarding the reliability surrounding the Euro Zone's apparent economic recovery.

A move represented by point B on the graph above which shows the subsequent Euro weakness that followed as the results from the European Bank Stress tests came in better than forecast.

These results actually had a negative effect on the Euro, as the reliability of what should have been seen as positive tests and results for the single currency were denounced as a political whitewash by a majority of financial experts, and saw confidence in the single currency drop significantly.

Despite improvements in Germany’s unemployment figures and improving economic and growth sentiment contributing to recent Euro strength, other Euro member states are not experiencing the same economic recovery.

A point recently emphasised by respected former Chief economist of the World Bank and Noble Prize winner Joseph Stiglitz who said that: “The different needs of countries with high trade surpluses, particularly Germany and those running deficits such as Ireland, Portugal and Greece meant that the single currency was under intense pressure and may not survive.”

Therefore, for all of the obvious concerns currently surrounding Sterling it seems hard to argue that the Euro is anywhere near as stable as recent market movement suggests and is by no means out of danger of collapsing in the medium term as financial concerns continue to engulf the Euro Zone.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.