Sterling/Euro Currency Review Q1 2011

Friday 15 April 2011

Sterling experienced significant losses against the Euro throughout the first quarter of 2011, but there is still some uncertainty for the Euro, writes Ben Scott.

A blend of poor economic data, negative sentiment and ever lowering potential for interest rate increases in the UK all lead to weakness for Sterling despite positive sentiment amongst traders coming into the New Year.

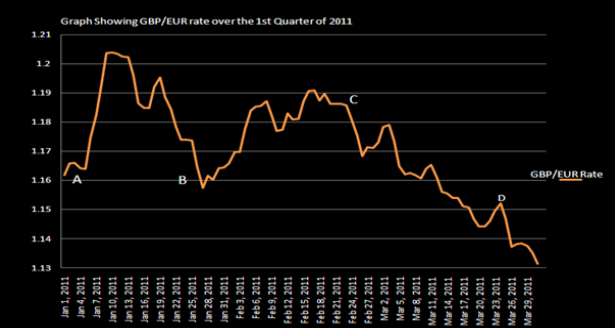

Sterling experienced a high of 1.2038 (interbank) against the Euro and a low of 1.1314 (interbank) in the period of Qtr1/11 as all positive signs surrounding Sterling were quickly reversed.

Despite the average GBP/EUR exchange rate increasing from 1.1636 (interbank) in Q4/10 to 1.1716 (interbank) in Q1/11, it is the continuous downward trend from mid January that will be causing the most concern for Euro buyers.

Movement throughout the first quarter has been largely dictated by interest rates expectations in the UK, but with a lack of agreement across the board this has lead to a very unpredictable period, particularly for GBP/EUR.

Support for Euro

The improvement of Sterling’s fortunes against the Euro immediately after Point A on the graph saw Sterling hit a 4 month high of 1.2038 (interbank). It came as a result of a combination of concerns surrounding the European debt crisis, and growing confidence that due to ever increasing inflationary pressures in the UK, the Bank of England would be forced to raise interest rates well in advance of the European Central Bank, expectations which added further strength to Sterling.

Many senior members of European countries made desperate attempts to support the Euro in this period, including a statement from the French Prime Minister that the “European debt crisis is not a crisis of the Euro, which remains a strong currency”.

Nevertheless, the writing seemed on the wall regarding Portugal’s battle with its debt obligations, as speculators predicted Portugal was no longer able to finance its financial obligations and the Euro weakened accordingly.

However, in an unexpected move, on 11th January, both China and Japan committed to and started buying bonds issued by the Euro-zone. They did so in an attempt to provide support to the beleaguered Euro. This proved immediately successful and saw significant recovery of the Euro in the following 2 weeks.

Despite Sterling’s positive movement in early January, Sterling gains were made amidst a backdrop of increasingly gloomy economic data in the UK, which saw declining construction, poor retail sales figures, and a massive 1.3% drop in house prices in December.

These negative figures accumulated with the announcement of a shock contraction in GDP, which at -0.5% for Q4/10 left the UK technically facing the potential of a double dip recession. As a result, towards the end of January GBP/EUR rates were lower than at the start of the month despite the European debt crisis.

Reversal of Fortunes

Immediately after Point B on the graph, Sterling weakness was significantly reversed as strong manufacturing data (which is widely seen as the cornerstone of any UK economic recovery), improved business sentiment and an upswing in the construction sector reduced fears of a double dip recession adding weight to the argument that poor weather in December was the key contributor to the negative GDP figure seen on January 25th.

This lead investors to once more speculate that the UK would lead the European Central Bank by increasing interest rates in the following few months, with the NIESR (National Institute of Economic and Social Research) speculating that the Bank of England would have to raise interest rates at least 3 times in 2011.

Speculations which appeared supported by comments from Bank of England Monetary Policy Committee members Andrew Sentance, Charles Bean and Martin Weale all suggesting interest rate hikes were necessary, with Andrew Sentance going as far as to say “Monetary policy would most likely need to be tightened (interest rate increased) faster and by more than the markets currently expect”.

This added greatly to Sterling strength as the higher the interest rate of a country the more investment flows into that currency.

In the period between Points B and C positivity surrounding Sterling would have lead to greatly higher GBP/EUR rates were it not for the extraordinary support and confidence from China for the debt-ridden Euro, and the ever improving economic figures from Germany, including a drop in the number of people claiming unemployment benefit to 7.4%, the lowest level since November 1992.

Showing that regardless of the economic and financial turmoil felt by many of the peripheral European countries (where unemployment for the Euro-zone as a whole still breached the 10% level), the powerhouse of the European economy was taking significant steps in its economic recovery, adding great support to the struggling Euro.

And Down Again

However, sentiment soon changed, and the GBP/EUR rate dropped once more, as illustrated from Point C onwards on the graph, as Bank of England Governor Mervyn King took an extremely dovish (negative) stance on potential interest rate hikes.

Mervyn King contradicted market views of imminent interest rate increases by saying “Some people are running ahead of themselves” after the market had priced in an 80% chance of interest rate increases for May 2011. Mervyn King stated that he had predicted (on several occasions) that inflation may well top 5% before steadily correcting lower without the aid of higher interest rates, leading to another period of Sterling weakness.

In complete contrast to the Bank of England, members of the European Central Bank adopted a more positive outlook on potential interest rate increases signaling the imminent increase of interest rates in an effort to deal with rising inflation. European Central Bank governor Jean Claude Trichet noted on the 4th of March that an interest rate increase at the start of April was a strong possibility, adding significantly to Euro strength, as did comments from ECB member Orphanides that “Central Banks should be pre-emptive on inflation”.

Outlook

Going forward, numerous factors will dictate the direction of GBP/EUR exchange rate, with the economic outlook for the UK still failing to establish a significant recovery, as austerity measures take their toll.

The UK economic recovery still seems significantly behind the curve compared to the Euro-zone, despite the financial crisis, which will undoubtedly see Portugal accept an EU financial bailout expected to be in the region of approximately €80 billion.

Austerity measures are really starting to bite in the UK. Despite three out of the last four months showing increases in house prices, rising unemployment, and announcements on the 31st March that Consumer Confidence has hit 20 year lows, combined with increases in mortgage defaults, undoubtedly point to a worrying period of economic and consequential Sterling weakness.

Furthermore, and as illustrated by Point D on the graph, George Osborne's budget for the UK announced on 23rd March failed to provide any support for Sterling, and the downgrade of UK growth forecast announced in the budget from 2.1% to 1.7% shows how depressed the UK economy remains.

Decreased growth forecasts lead to credit rating agency Moody’s announcing that the UK’s much revered AAA credit rating is now under threat. If the UK’s credit rating is cut it becomes more expensive to borrow money to run the country and will put Sterling under sustained pressure.

While the Bank of England Monetary Policy Committee still fails to agree on how best to deal with inflationary pressures, the European Central Bank moved on April 6th to increase interest rates for the first time since July 2008 to 1.25%, adding further strength to the Euro.

However, Portugal’s almost certain acceptance of financial aid from the EU raises the potential of contagion of the debt crisis spilling over into Spain. With unemployment levels over 20%, and an economy four times larger than that of Portugal, it would prove a massive threat to Euro stability if Spain were unable to finance its own debt burden.

This could have extremely negative impact on the Euro, and with estimates that a financial package if required to bail out Spain would cost €300+ million, it would lead to significant concerns that a bailout package for Spain would be too costly. In these circumstances the Euro’s survival as a single currency would be called into question, as Germany has already appeared reluctant to provide similar financial support to bail out European countries going forward, as it had previously done for Ireland and Greece.

Therefore, for all of the obvious concerns currently surrounding Sterling, the ongoing debt concerns of many European countries (particularly Spain) combined with the weakness of peripheral European countries which are likely to be exasperated further by interest rate hikes by the ECB at the start of April with several more expected throughout 2011, there is still great potential for Euro weakness during 2011.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.