Sterling/Euro Currency Review Q4 2011

Wednesday 01 February 2012

Sterling made significant gains against the euro in the final quarter of 2011, but it remains unclear if it can consolidate above €1.20, writes Ben Scott.

Despite the brief rally experienced by the euro on perceived positivity from the European debt crisis summit on 26 October, the lack of real information from the summit and the continuation of euro debt problems resulted in further predictions of a eurozone breakup in its current form.

Comments by former member of the Bank of England Monetary Policy Committee, David Blanchflower, who said of the European debt summit agreement, “this isn’t going to resolve anything” were fully vindicated. Sterling touched a high of 1.2009 (interbank) in December from a low of 1.1363 after the summit.

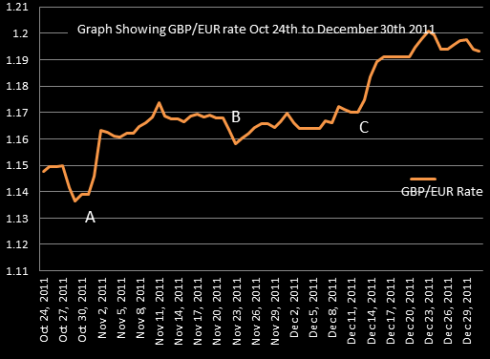

Despite a welcome increase in the GBP/EUR rate (as illustrated on the graph below), concerns remain for euro buyers as recent improvements are undoubtedly a result of euro weakness as opposed to any real Sterling strength, and could consequently be quickly reversed.

Greek Referendum

The sharp rise in the GBP/EUR rate after Point A on the above graph was undoubtedly as a result of euro weakness, but came despite increasingly negative economic fundamentals in the UK. The Bank of England’s Markets Director, Paul Fisher, stated that there was a “significant risk of the UK economy falling back into recession”.

Euro weakness was compounded going into November when, in an ill-conceived effort to pacify the Greek public, the Greek Prime Minister, George Papandreou, called for a referendum on whether or not Greece would accept the terms of the bailout package. This threatened to destroy months of work by the EU and sent the euro into further decline.

After further warnings from European leaders that “a referendum for Greece leaves them close to exiting the EU”, Papandreou signalled that he would no longer allow a referendum, but damage to the euro was significant.

Europe's New Technocrats

Following the period of euro weakness starting November, a period of stability continued to Point B on the graph (23 November), despite a glaring warning from British Prime Minister, David Cameron, who called for EU leaders to “act now or the single currency will fail”.

Weak economic factors early to mid-November in the eurozone saw German economic figures fall. Further, Italian bond yields exceeded the critical 7% barrier (the level at which Greece and Ireland had been forced to seek a bailout), and a European Central Bank (ECB) interest rate cut from 1.50% to 1.25% followed the first ECB meeting chaired by new Chairman, Mario Draghi.

The significant potential for euro weakness was offset by the resignation of Greek Prime Minister, George Papandreou, and the resignation of Italian Prime Minister Silvio Berlusconi. The replacement of these political leaders by economists, Lucas Papademos and Mario Monti respectively, settled the markets expecting greater austerity measures from the new leaders.

The euro produced some slight gains against Sterling from Point B onwards, as euphoria surrounding the recently settled governments willing to tackle their debt crisis continued to buoy the euro. Simultaneously, a period of anaemic economic data in the UK weighed heavily on Sterling.

As a consequence, Bank of England member Martin Weale admitted “there’s a strong case to ease policy further”, hinting towards more Quantitative Easing, which historically devalues a country’s currency when introduced.

David Cameron, contributed to this Sterling weakness, confessing that the UK is “well behind where it should be on growth”. However, this was quickly reversed on 21 November when the British government announced measures to stimulate the housing and building market sector in an effort to stimulate the UK economy.

Indications of the significant instability and headwinds faced by the euro were highlighted by the ECB’s decision at the beginning of December to further cut interest rates to 1% from 1.25%, reversing in two months the two interest rate hikes made earlier in the year. This emphasised the lack of agreement and unity which has debilitated the euro throughout 2011, a concern which looks certain to continue well into 2012.

Despite positive indications that Ireland and Italy were successfully implementing their austerity measures, credit rating agency Standard & Poor’s cited a warning on 5 December to six countries with AAA credit ratings in the Eurozone (Germany, France, Netherlands, Austria, Finland and Luxembourg), which kept the euro under sustained pressure.

Euro Summit

Euro weakness from Point C on the above graph highlights a reoccurring theme as market direction continued to be dictated by political events or a lack of political agreement as opposed to hard economic facts.

Following the initial optimism for the ‘Summit to save the Euro’ (9 December), the markets provided a damning verdict due to the resultant lack of clarity and commitment, with credit rating agency Fitch deriding the lack of decisive measures.

After failing to dictate its own direction, tension surrounding Sterling increased on the announcement that European leaders had agreed a budget and tax pact targeting the resolution of the European debt crisis ‘summit to save the euro’. However, the UK vetoed the scheme on the decision not to grant UK Prime Minister David Cameron’s request for an opt-out on financial regulations, leaving the UK on very shaky ground.

However, Sterling was soon on the front foot after poor eurozone economic data, combined with improved UK Producer Price Index figures, better than expected export figures and a reduction in the UK budget deficit. The deficit reduction suggests the UK’s austerity measures are working, a continuation of which is vital for sustained Sterling prosperity, but unfortunately very unlikely.

Outlook

Going forward, in the short to medium term the UK and Europe seem caught in a battle to see just who has the worst economic outlook.

Recent poor retail sale figures in the UK, house prices hitting 2½ year lows and unemployment reaching 15 year highs (and rising), contributed to credit rating agency Fitch admitting that, “Britain’s ability to retain its (vital and prized) AAA credit rating has been largely exhausted”.

If the UK experiences a cut to its AAA credit rating the effect on Sterling could be catastrophic as the cost of repaying UK debt increases significantly.

However, the gloomy UK outlook is matched by similarly negative prospects for the eurozone. Flagging economic fundamentals in Germany led to the German economy contracting 0.25% in Q4 2011, indicating the EU is once more standing on the edge of recession.

Whilst Sterling may experience some gains as a safe haven alternative to the euro, as our main trading partner, any European recession will have a negative impact on the UK economy, limiting the potential for gains against the euro.

Although it is easy to maintain a negative view on the euro as a result of the lack of harmony amongst political leaders, there is plenty of evidence that European leaders are pledging their commitment to tighter fiscal integration. Whether the markets are willing to give the required time to implement this is key in deciding whether the euro does indeed fail in its current format.

On a more positive note for the euro, the ECB has continued buying Italian bonds as a means of reducing Italian borrowing costs. However, forecasts from Citibank that the ECB will be forced to cut European interest rates in half from 1% to 0.5% by the end of June does provide continued uncertainty for the single currency, whilst indicating the severe headwinds that the ECB is faced with.

Of great concern for euro sellers will be comments from a German finance advisor that “a 50 per cent write down on Greek debt holdings would not be enough to save Greece from defaulting”, whilst a recent article in a German magazine stating that the “International Monetary Fund is losing confidence in Greece’s ability to work off its mountain of debt”, points to the potential for a rapid euro decline.

In spite of all of the obvious concerns currently surrounding both the UK and European economies, Prime Minister David Cameron’s decision to veto the EU treaty could prove the most costly factor for Sterling. Despite continued gains coming into 2012, seeing GBP/EUR hit a high of 1.2159, history shows that in recent years Sterling has struggled to consolidate any gains above 1.20.

All rates are quoted as interbank rates.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.