Sterling/Euro Currency Review August 2013

Tuesday 03 September 2013

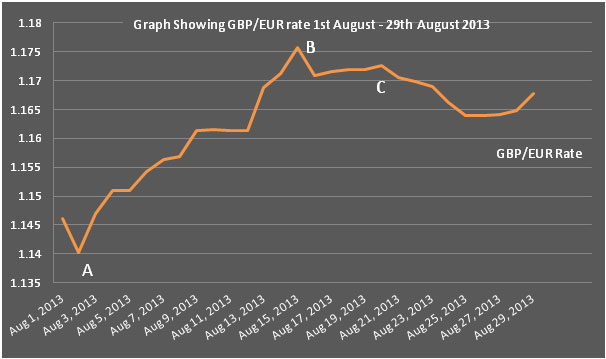

Sterling made positive gains against the euro in the month as economic data lead to speculation that the UK is experiencing a mini boom, says Ben Scott.

Sterling gains could have been even higher during this period were it not for improving economic data in the eurozone. German growth in Q2 2013 once more outperformed the rest of the eurozone, proving robust enough to allow the eurozone to finally emerge from recession.

Regardless of eurozone improvements, after previous months of Sterling underperformance euro buyers will feel buoyed by improving UK sentiment.

Sterling gains during this period came despite Bank of England (BoE) minutes suggesting further monetary stimulus remains a very real possibility - a concern emphasised by Bank of England Governor Mark Carney 28 August 2013 when he said “(the) Bank of England to consider more stimulus if financial conditions tighten or recovery risks falling short”. With monetary stimulus having a damaging impact on Sterling in the past, it is not inconceivable to conclude that any further quantitative easing would probably impact negatively on the recent Sterling gains.

Comments from European Central Bank (ECB) President Mario Draghi warning of “a slow recovery due to potentially weaker than expected domestic and global demand” kept the euro under pressure throughout August, despite improving economic data from most European countries. Meanwhile, the inability of EU nations to implement structural reforms as quickly as required could prove detrimental to the euro in the short term.

Exchange rates remained relatively static until point C, yet sentiment in the UK economy continues to improve. With already impressive growth figures for Q2 2013, revised even higher towards the end of August, supporting the Confederation of British Industry’s decision to raise their UK growth forecasts for both 2013 and 2014, further Sterling strength is a very real possibility.

Outlook

Despite BoE Governor Mark Carney using his ‘Flagship Policy’ forward guidance to indicate interest rates will remain low until 2016, investors feel this guidance is overly pessimistic, with market forecasts suggesting UK interest rates will have to rise as early as Q1 2015. Higher interest rates would, potentially, make Sterling a far more attractive investment.

Nevertheless, Mark Carney used his second public address on 28 August 2013 to rebut these market forecasts, reiterating that rates will not increase until unemployment drops below 7%. With unemployment rates expected to remain stubbornly above 7% for the foreseeable future, low interest rates for an extended period could prove damaging to Sterling.

Despite a period of improved economic data the euro outlook remains extremely unpredictable. Whilst improved economic data allowed the eurozone to snap 18 consecutive months of economic contraction, positive sentiment was reversed on the announcement that the ECB reduced overall growth forecasts for 2013 - suggesting recent improvements are far from sustainable. Growth downgrades from the ECB also negated positive euro sentiment created by EU member Olli Rehn who claimed, “the evidence is that the economy is gradually gaining momentum”.

Unemployment remains a significant hindrance for any maintainable economic recovery for the eurozone, but of more concern are comments from German Minister, Wolfgang Schauble, who hinted that Greece will require a further bailout before the end of 2014, in addition to the two bailout packages totalling €240 billion already received. If accurate, such forecasts would have an extremely negative impact on the euro.

With elections looming in Germany there is indisputable evidence that further financial support for indebted European countries is seen as politically toxic, with the German public clearly shifting to a policy of protecting self-interest. Current German Chancellor, Angela Merkel has, domestically, experienced growing opposition to a perceived weak-line approach regarding the indebted peripheral European countries, suggesting any further financial aid would struggle to find support should another European country fail, which although hypothetical, would potentially have ruinous consequences for the euro.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Reform of Auto-entrepreneur Stalled

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.