Sterling/Euro Exchange Rate Review August 2017

Friday 08 September 2017

On a trade weighted basis, August saw the worst performance in the pound since October 2016, with the UK currency softening against the euro for its fourth consecutive month, writes Ben Scott of FC Exchange.

Early August GBP/EUR Disappointment

The start of August was disappointing for the pound when only two members of the Monetary Policy Committee (MPC) voted for higher interest rates, following a faltering inflation reading for the first time since October.

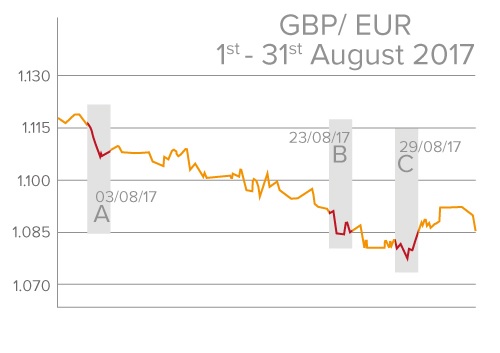

Sterling fell against almost every other major (point A) falling from 1.11 to 1.10 versus the euro, as the follow-up press conference saw Bank of England (BoE) Governor Mark Carney announce that British growth had been revised lower for both 2017 and 2018.

Meanwhile, the euro had a great start to August as unemployment in the currency bloc remained at an eight-year low.

Inflation and retail sales figures also surprised to the upside, and speculation mounted that the European Central Bank (ECB) would soon begin tapering its massive sovereign bond buying programme.

As the month continued, the pound sterling to euro (GBP/EUR) exchange rate hit a 10-month low (point B) and major institutions began to suggest that the currency pair was headed towards parity by the end of this year, or start of the next.

By the end of August, GBP/EUR had reached fresh eight-year lows of 1.0744.

UK Inflation

As August came to a close, the pound was on the back foot as inflation missed forecasts to rise and held steady at 2.6%. The number was significant as it relieved pressure on the Bank of England to increase interest rates.

Mounting inflation combined with weak wage growth has been squeezing British households; lethargic pay increases have been a headache for the Bank of England since the financial crisis.

On a more positive note, the UK’s unemployment level slipped to a 42-year low in August at 4.4%, which allowed the pound a little buoyancy.

Meanwhile, German growth rocketed to reach four-year highs while the Eurozone registered six-year highs. Eurozone inflation rose higher-than-expected to reach 1.5% in August, up from July’s 1.3%. The European Central Bank’s target is to have inflation reside close to, but below 2.0%.

ECB Quantitative Easing

As the European Central Bank looks to begin tapering its quantitative easing programme, investors are expecting President Mario Draghi to begin addressing the strengthening euro. The Jackson Hole symposium in August would have been a prime—not to mention expected—opportunity for the central banker to discuss QE, but as he avoided the topic completely, markets have been left wondering what’s next. The most recent ECB minutes stated that the policymakers were concerned that there was a ‘risk of the euro overshooting potential.’

As the Eurozone relies heavily on exports, a weaker euro is more beneficial for exporting nations and economists have suggested a stronger euro could be a hindrance to weaker nations in the currency bloc as they recover. The euro rose to a two-and-a-half-year high versus the US dollar (EUR/USD) in August after Draghi failed to talk down the currency and markets grew concerned about the impact of Tropical Storm Harvey.

Furthermore, while markets have been gearing up for the tapering of the ECB’s quantitative easing, there’s a shadow of doubt over the central bank’s timescales. If a strong euro continues to prevail, markets may have to wait before the ECB will adjust its sovereign bond buying programme for fear of how much damage a strong euro could have on the currency bloc’s recovery.

Brexit Shots Fired

The EU’s chief Brexit negotiator Michel Barnier fired a warning shot at Britain at the end of August, saying the UK needed to start negotiating ‘seriously’. The move saw investors sell-off the British currency as they priced in the possibility of a messy British exit which would be likely to be more damaging to the UK economy than the Eurozone should it occur.

Perhaps as the UK navigates its way out of the European Union, markets will become accustomed to negotiations pressuring the pound lower.

Since the vote, Brexit has certainly pushed sterling lower, but the lack of progress is proving to be very damaging too.

As a result of poor progress in August with negotiators at loggerheads, the British currency had a lacklustre start to September, hovering above the lowest levels seen in eight years.

US/North Korea

The world has been watching geopolitical tensions escalate between the US and North Korea, and investors have headed for safe-haven currencies on several occasions when in risk-off mode.

Interestingly, the euro emerged as a safe-haven currency along with the Swiss Franc (CHF) and Japanese Yen (JPY) last month as markets favoured the single currency in the face of conflict across the Pacific.

If tensions deepen, it’s likely that the US dollar will fall, and the euro could rise.

German Elections

Not only are Brexit talks due to resume for their fourth round in September, German Chancellor Angela Merkel will discover whether she’s been successful in her bid to remain in power for her fourth term. Angela Merkel has been in power for the past 12 years and polls are suggesting she’ll remain in control when the September 24th vote takes place. Meanwhile, Brexit talks are scheduled to open for their fourth round on the 18th September.

Outlook

Brexit will remain a heavy weight for the pound, but central bank comments will also have significant sway on exchange rates in the near future.

Thursday September 14th will be an interesting day for sterling movement with the latest Bank of England interest rate decision and meeting minutes, while Thursday 7th September will see the European Central Bank make its September rate decision and hold its follow-up press conference. While markets expect the ECB to maintain its 0.0% interest rate, investors will be keen to hear what the central bank has to say regarding its asset purchase programme.

In terms of economic data, UK inflation and unemployment rate numbers are out mid-September which could be major catalysts for pound movement, while GDP growth rate figures could offer sterling some opportunity to fluctuate at the end of the month. Eurozone growth figures will make their way into the spotlight on 7th September.

While the German Federal elections could cause some movement, it’s likely if Merkel wins as forecast, the single currency will strengthen on political stability. There were rumours Italy would call a snap election so that it was in line with Germany’s voting schedule, but after the deal between Italy’s prominent political parties regarding electoral reform fell apart, that’s now very unlikely. It was argued that a snap election could create further political instability — something that’s similarly been witnessed in the UK.

Meanwhile, North Korea will also play a huge role in risk sentiment and exchange rate movements in coming months. If tensions settle high-yielding currencies may be favoured, but if tensions continue to rise the euro could be offered some more support.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.