Sterling/Euro Currency Review Dec 2015

Wednesday 06 January 2016

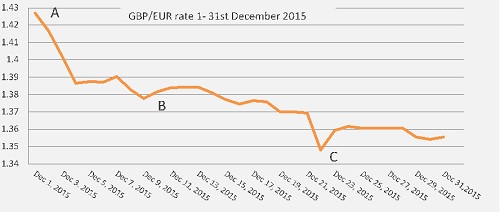

Sterling found itself under significant pressure against the euro in December, falling to a 10-week low of €1.3480, whilst trading at an average rate of just €1.3775 for the month, says Ben Scott.

Despite a GBP/EUR high of 1.4270 (interbank throughout) to start the month, - approximately 10% higher than the highest level seen in December last year - sterling soon came under a period of prolonged pressure as forecasts for a UK interest rate hike were pushed further into the future.

This was particularly emphasised by the newest member of the Monetary Policy Committee (MPC), Gertjan Vlieghe, who warned that tightening monetary policy was a big step and that he believed “UK growth needs to pick up or at least stabilise before this [interest rate increase] was even taken into consideration.”

With interest rates set to remain at record lows for the foreseeable future sterling is becoming a far less attractive investment.

Economic data from both the UK and the eurozone remained mixed as we have seen in recent months. The significant decline of GBP/EUR (between points A and B on the graph) was as a result of the European Central Bank (ECB) announcing a far smaller revision to their Quantitative Easing (QE) programme than anticipated, especially given recent disappointing economic growth and deflationary pressures in the Eurozone.

The ECB made a slight cut to the deposit rate from a previous level of -0.20% to -0.30%, making it more expensive for banks to hold money with the ECB in the hope that this would boost lending and therefore economic growth.

The ECB also extended the duration of their quantitative easing programme by six months, extending its end date from September 2016 to March 2017, which clearly fell below market expectations, with most predictions forecasting a significant increase to the ECB’s €60 billion-a-month bond buying programme. The fact this increase of ‘new money’ failed to materialise meant the euro was not further devalued, allowing it to make instant gains of almost 2% against the pound.

Further sterling declines, from point B, came as a result of the Bank of England again indicating that inflation is expected to remain below 1% until at least the end of Q2 2016, and significantly below the target level of 2%, for the foreseeable future.

This again makes sterling a far less attractive investment, but maybe more importantly, raises questions regarding the credibility of the Bank of England’s forecasts which had initially predicted a return to 2% for inflation six months ago.

With oil prices still extremely low and helping to keep inflation low, a return to 2% before 2017 looks extremely unlikely, further reducing the prospect of an interest rate hike in the UK in 2016.

Whilst positive retail sale figures for November and the release of the UK’s unemployment rate, (which fell to 5.2%, the lowest level since January 2006) provided some respite for sterling, the downward trend was soon re-established with GBP/EUR reaching 10-week lows as illustrated by point C on the graph.

Data released at this time showed UK borrowing rose 10% in November compared to the same the previous year, raising concerns about the finances of the UK, whilst bringing doubt to Chancellor George Osborne’s target of turning the nation’s deficit into a surplus by the end of the decade. This pushed sterling lower against most currencies.

Outlook

Whilst important UK PMI service sector data for November proved positive (off-setting disappointing manufacturing and construction sector readings for the same period), it is worth noting that the report does highlight some fears. It suggests that there is some concern surrounding the long-term outlook for the service sector if inflation remains low for an extended period, which, for the time being, seems to be the case.

Disappointing service sector readings would weigh heavily on UK GDP readings and would have a negative overall impact on the whole UK economic growth, which would be detrimental to the pound through 2016.

Euro was boosted by the announcement that unemployment is down to 10.7 % and, whilst this remains a statistic of great concern, 10.7% represents the best reading since the end of 2012 and with further improvements expected in this sector, further raises the prospect of euro strength.

Despite claims from Prime Minister David Cameron in December that “a pathway to a deal” on Britain’s continued membership of the EU had been established, press releases soon revealed such claims were extremely optimistic, and potentially misleading, with most demands from the UK likely to be rejected by the EU.

Indicators now forecast that support for Britain leaving the EU is growing to record levels with current support over 40% for the UK to leave the EU.

Whilst any referendum is unlikely to take place before 2017, such support for the UK to leave the EU will undoubtedly create uncertainty throughout 2016, which now looks set to be an extremely volatile year for sterling.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Parcel Delivery Price Ring

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.