Uncertainty Causes Sterling to Soften

Friday 06 January 2017

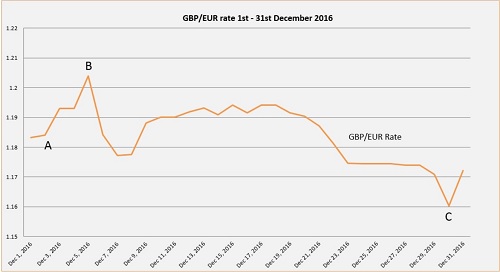

December was a mixed month for the GBP/EUR exchange rate with sterling generally tapering lower under pressure from Brexit concerns, writes Ben Scott.

GBP/EUR reached a short-lived high of 1.2040 at the start of December, but the rest of the month and festive season saw sterling soften.

The month began with the UK currency falling against major counterparts after the Organisation for Economic Co-Operation and Development (OECD) predicted a fall in UK growth in coming years (point A). The OECD’s prediction even undercut the Bank of England’s (BoE) growth forecasts, coming in at 1.2% for the year.

However, the pound to euro exchange rate was allowed some support following the release of the Bank of England’s (BoE) Financial Stability Report which managed to maintain a positive stance. The central bank noted that although Brexit has caused uncertainty with regards to economic growth etc, the UK economy has remained resilient, despite the political challenges taking place. Investor sentiment in the pound declined ahead of the release, but increased after the market had digested the BoE’s statement and then offered a backbone for sterling to gain.

Meanwhile, markets eagerly watched developments in the Brexit Supreme Court appeal, which started on the 5th December and caused further concerns as to when Article 50 could be triggered.

The euro had problems of its own as December began, with the Italian referendum shaking sentiment as political instability took hold of the currency bloc. The GBP/EUR exchange rate was able to climb to a four-month high at 1.2041 (point B) as markets edged away from uncertainty, only to fall back lower to the region of 1.1800 later in the session.

The referendum was put forward by Italian centre-left political party Prime Minister Matteo Renzi, as he asked citizens to vote on whether they would approve a new constitutional law to reform the powers of the Italian parliament. Renzi announced his resignation after three years in the role of Prime Minister after the Italian people failed to vote in favour of the bill and instead opted to keep Italy’s historic political system.

With the ‘No’ vote prevailing, the door has been left open for far-right political parties which have increased in popularity in recent years amid economic stagnation and migration issues. The year saw some surprising political twists the world over, which suggests citizens are desperate for change, and in turn has translated into extreme market volatility and uncertainty.

The pound began to weaken against the euro and the US dollar following the release of disappointing UK retail sales figures (point B decline). Year-on-year, the ecostat fell from 1.7% to 0.6% in November, despite economists’ forecasts to remain static.

In other data, the UK’s consumer price index (CPI) showed that the nation’s inflation had increased above predictions. November saw the core annual reading climb from 1.2% to 1.4%, while the non-core measure jumped from 0.9% to 1.2%. With the rise came comments that the weak pound posed a high-inflation risk which could result in measures being taken to accommodate the economy. Additionally, the UK’s ILO unemployment rate remained at 4.8%.

As the month continued UK economic data started to taper off in the run-up to the festive period. Point C shows a dip in the GBP/EUR exchange rate which came following global developments and EUR strength against other majors such as the US dollar (EUR/USD).

The US dollar had a positive December in its currency pairings with only a bit of a set back in terms of profit taking at the end of the month. The US Federal Reserve hiked interest rates at the start of the December in line with expectations and the buoyant buck remained a strong contender in the market, causing weaker currencies to fall against it.

Outlook

The pound to euro currency pair could be in for an interesting start to the year with a host of events ready to destabilise the market.

Brexit developments will continue to weigh on sterling uncertainty and the market will be watching for the Supreme Court announcing its ruling on January 17th.

The recent resignation of Sir Ivan Rogers as the UK’s ambassador to the EU caused the pound to soften as the event showed how volatile the negotiations could be and heightened concerns for a ‘hard Brexit’.

It seems as if for the foreseeable future, sterling volatility will be at its most prominent, despite some favourable figures making their way onto the scene.

There are some key pieces of economic data coming up for the UK in January, including the latest balance of trade stat on Wednesday January 11th and inflation rate numbers on Tuesday January 17th. Inflation has been forecast by some economists to rise from 1.2% to 1.3% and, if correct, could cause the pound to rally against other majors.

Meanwhile, the euro is also set for an interesting January as the currency bloc is left at the weakness of its own political developments.

In the lead-up to the French presidential elections it is expected that there will be some major movement as the nation may choose to vote for far-right Front National leader Marine Le Pen. Although previous polls have suggested that she’s less popular than conservative front runner Francois Fillion, political surprises aren’t in short supply of late, d so it’s possible that the euro could be in for a bumpy ride.

Marine Le Pen has stated that she believes France should leave the currency bloc, and investors will be keeping a close eye on polls in coming months to try and determine the Eurozone member’s fate.

Wednesday 11th January could witness GBP/EUR fluctuations with German gross domestic product (GDP) numbers making their way onto the scene, followed by the European Central Bank’s (ECB’s) monetary policy meeting accounts released on Thursday.

The US dollar may experience its own turbulence in January as Inauguration Day nears and president-elect Donald Trump takes centre stage as US leader. His actions and comments are likely to play havoc with the dollar as the markets adjust to a new leader. However, at this point it’s difficult to predict which way the buck may swing.

In terms of January economic data, the US unemployment figure increased in December from 4.6% to 4.7%, but wage growth rose positively from 2.5% to 2.9% on the year. Friday 13th January will see the publication of US advance retail sales numbers which are likely to influence the way the greenback trades quite significantly. Economists are expecting December to show a 0.50% reading following the previous month’s 0.10%.

Long-term the markets will be carefully eyeing global changes – Germany has several high-profile elections taking place this year and the UK will be making more progress on its departure from the EU. Additionally, the new US president is likely to cause movement in the markets as policy changes occur and markets adapt to economic developments.

If you’re looking at trading currency in 2017 for a property purchase, take time to speak to a broker who can help you manage your FX risks.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Business Rates Relief

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.