Sterling/Euro Currency Review January 2015

Tuesday 03 February 2015

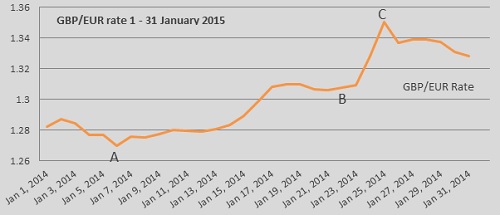

After a positive end to December, Sterling experienced a mixed start to January before reaching the highest level since 2008 against the euro, says Ben Scott.

The euro was devastated by a combination of:

- the Swiss National Bank giving up protecting the euro/Swiss franc floor at 1.20 (interbank throughout);

- the European Central Bank (ECB) finally announcing a full quantitative easing programme to deal with weak economic growth and deflation;

- the elections in Greece.

The far left anti-austerity Syriza party in Greece, which won the election, caused immediate concern that Greece would negate on its previously agreed bailout terms, thus putting the country on a collision course with the 'Troika' and the rest of Europe.

All of these factors combined to create fresh seven-year-high for GBP/EUR as illustrated by point C on the graph below.

After Sterling had reached six-year highs coming into the New Year, early January saw the pound start to slide on the back of deteriorating economic data, which including poor construction figures and a disappointing reading in the all-important PMI services data, indicating the slowest pace of growth for 19 months in December.

This raises major concerns for the UK’s economy as the service sector accounts for approximately 78% of gross domestic production and three quarters of all jobs in the UK, and resulted in a month-low of 1.2698 on 6 January 2015 (point A). January saw GBP/EUR trading at an average rate of 1.3006.

Initial Sterling losses against the euro coming into January would have been significantly worse were it not for the announcement that inflation in the Eurozone had turned negative in December, raising questions on ECB policy. James Ashley (Chief Economist at RBC Capital Markets) stated that: “In our view, the inconvenient truth for policymakers is that in large part (deflation) is a reflection of the failure of policy, both fiscal and monetary.” With deflation confirmed intervention from the ECB becoming a certainty, it resulted in euro weakness.

The shock decision of the Swiss National Bank on 15th January to give up on the EUR/CHF floor of 1.20 saw the Swiss franc experience an immediate gain against most currencies - almost 25% against sterling and nearly 30% against the euro. Euro weakness, however, was compounded in the aftermath of this decision by an accompanying statement from the Swiss National Bank stating: “Recently divergences between the monetary policies of the major currency areas have increased significantly, a trend that is likely to become even more pronounced”. This provided a clear indication that the Swiss National Bank (SNB) expected the ECB to announce quantitative easing imminently.

For an extended period investors have been asking when the ECB would introduce a full programme of quantitative easing to deal with falling levels of inflation and poor economic growth and this question was finally answered on 22nd January when ECB President, Mario Draghi, announced a massive QE boost to the Eurozone, with a plan to pump an additional €60 billion per month from March 2015 until the end of September 2016 (and possibly longer) directly into the financial markets in an attempt to stimulate spending and boost economic growth.

Whilst quantitative easing appears to have been a great success in stimulating economic growth when introduced in both the UK and more recently the US, the immediate effect on the euro was negative.

The basic principle of supply and demand saw the euro slip into freefall on the announcement of a QE plan far larger than many expected, with the ECB pledging to flood the markets with at least €1.1 trillion.

After a difficult two weeks for the euro, the worst fear of the Eurozone was realised when, as expected, the far left anti austerity Syriza party won the Greek election. The immediate aftermath saw GBP/EUR reach seven year, pre-recession highs of 1.3503.

The Syriza party had campaigned on renegotiating the terms of the €240 billion EU-IMF bailout, which imposed strict spending and taxation rules on Greece, a point the Syriza party claimed significantly contributed to the Greek economy shrinking by 25% since the onset of the financial crisis, diminishing national pride.

Markets are concerned that the election of the Syriza party threatens to plunge Europe deeper into crisis as any further bailout payments to Greece are likely be withheld. Indications suggest Greece has enough money to function until the end of February when, unless an agreement is reached, there is a strong probability that Greece will default on its debt. This could force Greece to leave the Eurozone, driving Europe into an even deeper crisis, which would in turn reignite the contagion that blighted the Eurozone throughout 2012.

Outlook

Whilst Bank of England Governor, Mark Carney, has attempted to put a positive spin on falling inflation in the UK, by claiming the recent fall in oil prices is “net positive for UK growth”, lower inflation has seen expectations for a Bank of England interest rate hike now pushed back to the middle of 2016, making Sterling far less of an attractive investment.

Whilst sterling has benefitted from ongoing problems in the eurozone, recent data has missed expectations, raising concerns of the UKs ability to add to economic growth seen last year.

Overall, the ECB’s plan to inject at least €1.1 trillion worth of new money into the distressed eurozone economy should, in theory, result in businesses and people borrowing more and therefore spending more, which would boost the economy and strengthening the euro in the medium to long term.

Elsewhere, peripheral European countries will be monitoring the progress of Greece in renegotiating the austerity measure put on them as a result of the bailout. Successful negotiations in reducing the debt or agreeing more favourable terms will surely encourage other European countries who are following austerity as a result of a bailout to seek more favourable terms, which would result in significant debt write-downs heaping further pressure on the euro.

After initially falling on the back of the election of the Syriza party the euro did find some support when New Greek Prime Minister, Alexis Tsipras, claimed his country “will not default on its debt”. Prime Minister Tsipras also stated, “We won’t get into a mutually destructive clash, but we will not continue a policy of subjection."

‘Compromise’ seems to be the key word in debt negotiations and positive results will prove vital for the existence of the euro in its current form.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: UK Pension Changes

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.