Trump, Brexit, and Elections Threaten GBP/EUR

Monday 06 February 2017

January was one of the most volatile political months in recent memory and the fallout has left the currency market shaken, writes Ben Scott.

Sterling has been a yo-yoing against other major currencies as geo-political events have taken place, leaving many to wonder what the fate of the pound, euro, and US dollar may be.

The pound to euro (GBP/EUR) exchange rate jumped between levels of 1.1291 and 1.1834 last month, while the sterling to US dollar (GBP/USD) experienced movement between 1.1992 and 1.2668.

Trump Presidency

Since his inauguration last month President Trump has successfully managed to allow his disapproval rating to surpass the 50% mark in a record eight days. In comparison, former record holder Bill Clinton was in office for 573 days before breaching the 50% threshold. President Tump has so far led one of the most controversial presidencies seen for some time. Marches, global protests, and lawmakers standing their ground against Executive Orders have all occurred in January and shown that the political front in the US is incredibly unstable – a factor that can spook investors and lead to extreme market volatility.

Global leaders and politicians have spoken out against Trump’s Executive Order to prevent immigration from seven countries. European Council President, Donald Tusk, also wrote a letter to European leaders suggesting that Trump is a potential threat to the EU, along with Russian aggression, Chinese assertiveness, and global terrorism, stating: ‘For the first time in our history, in an increasingly multipolar external world, so many are becoming openly anti-European, or Eurosceptic at best. Particularly the change in Washington puts the European Union in a different situation; with the new administration seeming to put into question the last 70 years of American foreign policy.’

As American politics seep to all the corners of the world and concerns grow, the market is likely to remain extremely volatile.

Brexit

Moreover, Brexit continues to dominate UK headlines and financial markets are continually trying to guess what’s likely to happen next.

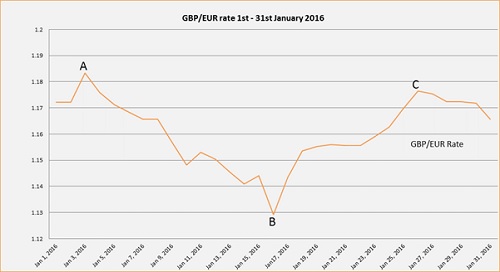

The pound had a great start to the month as published data revealed that UK manufacturing had risen to its highest level since June 2014 in December (point A). The rise was attributed to overseas buyers finding UK goods more attractive following sterling’s 2016 decline. However, GBP was offered little support when it was announced that Britain’s EU ambassador Ivan Rogers was quitting early, despite being due to leave much later in 2017.

Sterling dropped against other major currencies on the 15th January ahead of Theresa May’s Brexit speech (point B). Sterling hit its lowest level in over three months against the dollar and the weakest level against the single currency for two months. Overall, since the June referendum, the pound has weakened by around 20% and registered lows that were last seen regularly in 1985. Immediately after Theresa May’s much anticipated speech, which outlined her 12 Brexit objectives, GBP began to rally by almost 3% against the US dollar and over 1.5% against the euro.

The UK Supreme Court also determined that the triggering of Article 50 will need to have the backing of parliament and this offered the pound some temporary gains.

Furthermore, the Bank of England (BoE) announced that household borrowing had increased at its slowest pace since May 2015. The pound fell as speculation circulated that UK consumers were reining in their spending as fears for the outlook of the economy grew and household incomes came under pressure from rising inflation.

Economic Data to Impact Sterling

UK inflation rose from 1.2% to 1.6% in December - jumping above economists’ forecasts. Meanwhile, in the Eurozone, January’s flash reading of inflation jumped from 1.1% to 1.8% on the year. German inflation alone is residing at a preliminary 1.9%, which has fuelled views that the European Central Bank’s (ECB’s) quantitative easing (QE) needs to be curbed.

Following this, on the 31st January sterling rose against the US dollar when Trump slated China and Japan for ‘playing the money market’. In addition, Trump and his trade chief Peter Navarro accused Berlin of taking advantage of the ‘grossly undervalued’ euro to ‘exploit’ the US and the rest of the European Union. Furthermore, Navarro suggested that Germany was a ‘big obstacle’ in determining a trade deal between the US and the EU. As a result, the pound managed to register its best January in six years versus the US dollar.

Future GBP/EUR Forecasts – Short Term

In the short term, investors will be questioning whether the Bank of England (BoE) will increase UK interest rates as a result of a stronger pound. In the meantime, politics are likely to be the main source of movement for GBP/EUR. Since parliament supported the bill to trigger Article 50 it appears as if Theresa May should be on target to set the Brexit wheels in motion by March 31st as planned.

Prime Minister May headed to Malta at the start of February to attend the EU Presidency Summit in Valletta and to discuss both Brexit and migration. Ahead of the visit Maltese Prime Minister Joseph Muscat had stated that May must decide whether Britain’s fate lay with Trump and the US, or Europe.

Muscat stated: ‘I do believe the UK is in a very delicate situation, right now. It is fetching a free trade deal with Europe and eventually, the United States. In both trade deals it will be the junior partner because the UK is much larger than most European states, but it is smaller than Europe as a whole and smaller than the United States. I think it a balancing job the Prime Minister must make. I will not judge her on the choices she makes. But it is pretty clear she needs to choose her priorities well.’

Pound Sterling to Euro Outlook – Long Term

Over the next few years' investors will be keeping an eye on the UK’s trade performance as deals are negotiated with the EU27 and other nations further afield. The upcoming elections in France and Germany will certainly give some insight on what the UK’s bargaining position may be. Investors in the euro need to keep a close eye on developments in France in the next few months as we get closer to the election, which could potentially put the country on course for its own EU referendum.

In terms of global politics, the unpredictability of President Trump could cause the US dollar to become a wildcard in the market. If investors are spooked by actions undertaken by the world’s biggest superpower, it’s possible safe-haven assets like the Japanese Yen and Swiss Franc will rise. Alternatively, investors could favour commodities such as gold instead.

The Bank of England has suggested that the UK economy will slow over the next couple of years, despite upping its growth forecasts for 2017 several times since the Brexit referendum. If UK growth slows, the pound is likely to slip lower. The GBP/EUR decline could be even more pronounced if this year’s French and German elections run smoothly and right-wing parties miss out on leadership positions. However, if citizens in the euro area begin to favour right-wing parties who offer EU referendums, the euro could reach lows we haven’t seen for some time as there’s potential for the currency bloc to begin disintegrating.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Ups and Downs of Ski Property Prices

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.