Sterling/Euro Currency Review May 2014

Tuesday 03 June 2014

May saw Sterling make gains against the euro as a result of positive economic growth forecasts and that, with inflation in the UK stabilising at around 2%, there is greater potential to soon raise interest rates, says Ben Scott.

James Knightley, economist at ING Financial Markets, suggests that the “Bank of England’s first hike will probably come in February, but given the strength in growth, employment and asset prices the risks are skewed towards a slightly earlier move”.

Such projections do, however, contradict comments from Bank of England Governor, Mark Carney, who reassured borrowers that the bank rate would be “likely to remain at record low of 0.5% for some time”.

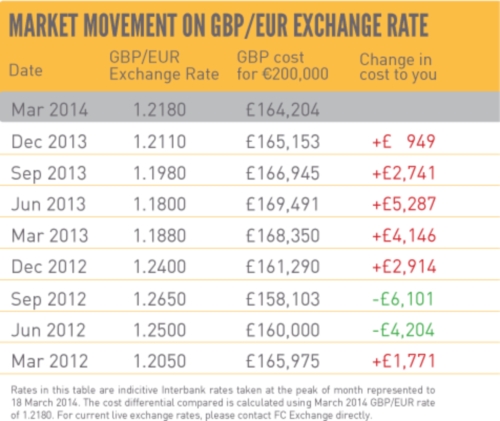

Growing speculation that the Bank of England could now rise interest rates as early as Q1 2015 is good news for euro buyers as higher interest rates would make Sterling a far more attractive investment, allowing Sterling to reach fresh 16 month highs against the euro above €1.23 (Interbank).

Sterling was boosted early in May by above forecast manufacturing and service sector data, as well as employment data showing the highest level of job creation since October 2013.

Gains were also supported by the OECD, which again raised the growth forecast in the UK for both 2014 and 2015, whilst simultaneously cutting global growth forecast. This suggests economic improvements in the UK are both robust and sustainable.

Economic data throughout the Eurozone continues to disappoint with all of the main countries within the single currency (Germany, France, Italy and Spain) seeing a decline in production.

Concerns of a deteriorating economy were emphasised by French Finance Minister, Michel Sapin, towards the end of May who, when addressing France’s National assembly, did little to support the euro. He further forecast that French economic growth will be just 1% in 2014, rising marginally to 1.5% in 2015, highlighting the fact that Europe’s second largest economy will remain a drag on the Eurozone’s economic recovery.

Of more immediate concern, however, are the signs of deteriorating economic activity from Germany, which has previously provided the vital foundation for the vast majority of economic improvements in the Eurozone. German industrial production proved extremely disappointing while the ZEW economic survey showed a significant decline in economic forecasts, adding further pressure on the European Central Bank (ECB) to take measures to boost the economy and tackle falling inflation. Should this happen, it would almost certainly prove detrimental to the euro in the short-term.

Euro declines during May can be traced directly back to comments from ECB President Mario Draghi who, when addressing the strength of the euro, said it was “cause for serious concerns”, adding to the growing indication that the ECB may intervene to devalue the euro further.

Mr Draghi went on to contribute significantly to euro weakness stating that the “Governing Council is comfortable with acting next time”, suggesting that the ECB are likely to either cut interest rates from already record lows of 0.25% or to move to a negative deposit rate, which means banks have to pay to hold money with the ECB. Either option would make the euro a far less attractive investment, with further euro weakness almost certain to follow.

Outlook

Numerous factors will determine the short-term direction of GBP/EUR rates. Sterling has been boosted by positive economic data including UK retail sales figures, which saw the strongest annual gain for 10 years whilst Gross Domestic Production figures continue to report solid growth throughout the UK economy. However, as cautioned by BOE Governor Mark Carney, “the (housing) market represented the biggest risk to financial stability and the long term recovery”.

With concerns that the UK housing market is overheating, Sterling could come under increasing pressure.

Whilst markets consider it a near certainty that the ECB will decide to cut interest or deposit rates (or potentially both) in June, there has been ongoing talk that the ECB may also introduce some form of quantitative easing. Reports now claim that the ECB is set to launch a €200 billion stimulus programme aimed at boosting the economy and protecting against deflation, and while this could prove positive to Eurozone economic growth, the short-terms effects could prove devastating to the euro.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: French Property Ownership Options

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.