Sterling/Euro Currency Review Nov 2015

Thursday 03 December 2015

November proved to be another positive yet volatile month for euro buyers as sterling continued recent gains against the euro, despite a downgrade in both UK inflation and growth forecasts from the Bank of England, says Ben Scott.

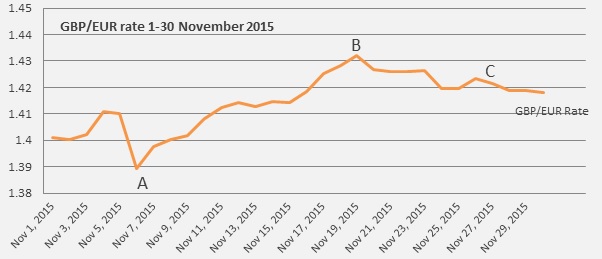

These downgrades added further support to the belief that UK interest rates will remain at record lows until at least 2017 and resulted in a decline for sterling with GBP/EUR trading at a month-low of 1.3893 (point A on the graph below).

Sterling was boosted by improved economic data in November, but it was undoubtedly concerns surrounding the prospect of an increase and/or extension of the European Central Bank’s (ECB) quantitative easing programme which would prove detrimental for the single currency. It undoubtedly acted as the catalyst for further euro weakness, which lead GBP/EUR close to fresh eight-year highs ahead of the ECB announcement due on Thursday 3 December.

Despite ongoing anxieties surrounding current UK inflation issues, GBP/EUR was able to reach a high of 1.4319 (interbank throughout) 19 November as illustrated by point B, with GBP/EUR trading at an average rate of 1.4145 throughout November.

Sterling started the month positively with signs of improvement in the construction sector, service sector and manufacturing sector, highlighting a significant improvement in UK domestic recovery and indicating sterling could enjoy improvements against its trading partners going into 2016.

Simultaneously the euro continued to depreciate against most currencies, hampered by disappointing economic data from Germany with factory orders, industrial production and economic confidence all providing a negative outlook.

Both the ECB and Bundesbank will undoubtedly be concerned with negative data from the largest and most significant economy in the eurozone falling, and whilst this does increase the prospect of further quantitative easing, which would prove negative for the euro. It also puts the ECB on a collision course with Bundesbank who maintains interest rates around 0% for a prolonged period, is starting to have a negative impact on the German economy, but with inflation in negative territory and muted economic growth across the eurozone, the tools available to the ECB seem limited.

Leading to high point B on the graph, sterling was boosted by positive employment data, which showed unemployment dropped to 5.3% with the level of employment in the UK at record highs.

Euro weakness and the catalyst for the GBP/EUR month high, however, came from the ECB Monetary Policy Committee, which gave a clear indication that the prospect of the eurozone missing its target inflation rate has increased. President Mario Draghi stated that, “If we conclude that the balance of risks to our medium-term price stability objective is skewed to the downside, we will act by using all of the instruments available within our mandate”. This represents the clearest indication yet, from Mario Draghi, that he supports the potential of slashing deposit rates and extending quantitative easing, which sent the euro into a tailspin.

Sterling gains were muted for much of the second half of the month leading to point C. Disappointing retail sales figures from the UK lead to speculation that the BOE may be forced to consider extending its’s own quantitative easing programme. Although Bank of England Governor Mark Carney indicated an extension to the quantitative easing programme could theoretically resolve the problem, it may not be the optimal solution. Nevertheless, as previously seen, the mere mention of quantitative easing had a negative impact on sterling as the introduction of more quantitative easing would make sterling far less attractive from an investment perspective going forward.

Outlook

A grilling for Bank of England governor Mark Caney and his colleagues by the Treasury Select Committee saw sterling drop early in November and whilst sterling losses were quickly recovered, comments confirming that low inflation (currently at -0.1% versus a target of 2%) was directly linked to low oil prices.

With no immediate signs of recovery, this provides the clearest indication yet that the potential of the Bank of England raising interest rates from current, record, lows remain slim for 2016. Interest rates, therefore, will almost certainly remain low for some time making sterling a far less attractive investment.

Meanwhile, concerns surrounding sterling’s ability to remain at current levels were further compounded by comments by BOE Chief Economist, Andy Haldane, who hinted at a growing prospect that interest rates could actually be cut due to “global headwinds” and weak inflation, which, if proved correct, would almost certainly be detrimental to the strength of sterling.

As highlighted by European Central Bank President, Mario Draghi, several times throughout November, the eurozone remains under significant downside pressure. Deflationary pressure continues to weigh on the euro as does concerns regarding movements from the Chinese stock market, which, whilst not directly linked to the euro, damages global confidence. This, in turn, when combined with a deceleration in global trade and growth, weighs heavily on the euro.

Whilst President Draghi has hinted that the ECB quantitative easing programme could run beyond September 2016 or even be increased in volume as previously forecast, any such announcements - expected 3 December - will likely prove damaging for the euro in the short term.

Elsewhere, Greece remains close to the headlines. A clash between Greek Ministers and creditors over the terms of the next tranche of aide worth €2billion, signals a potential return to the ongoing Greek debt saga.

Contention grew regarding creditors’ demands surrounding primary residence foreclosures. Whilst this issue has largely been agreed in the short term, it does highlight remaining fractions, suggesting another financial crisis is never far away and could potentially be a significant factor over the course of the next year.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Building Construction Costs

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.