Sterling/Euro Currency Review Oct 2015

Wednesday 04 November 2015

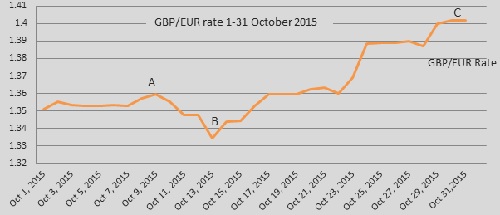

October proved to be an extremely volatile month for euro buyers as sterling recovered from a disappointing start to the month, to touch 10-week highs against the single currency, says Ben Scott.

Sterling started the month on the back foot as economic data from the UK continued to disappoint, further reducing the prospect of an interest rate increase in the near future.

Meanwhile concerns continued to grow that the next move from the Bank of England Monetary Policy Committee (MPC) might be to cut interest rates to deal with the threat of deflation, which would make sterling a far less attractive investment.

Despite ongoing anxieties surrounding the UK economy, the headwinds being experienced by the Eurozone meant GBP losses were quickly reversed leading to a GBP/EUR high of 1.4020 (Interbank throughout) as illustrated by point C on the graph.

This high came after an extended period of instability for sterling which had seen GBP/EUR trade at the lowest level since May 2015 when hitting a low of 1.3344 (point B). GBP/EUR traded at an average rate of 1.3641 throughout October.

As has been the case in recent months, sterling weakened during the first half of the month as disappointing economic data in the form of construction and service sector data both missed forecast, adding to concerns that the UK economic recovery continues to slow. It is, however, a further decline in the UK manufacturing sector in September, reporting the worst quarter in two years that epitomises concern for the short term prospects of the pound.

Manufacturing job losses were reported for the first time since April 2013, raising concerns that the recent GBP strength is having a detrimental impact on exports, whilst making further sterling strength highly undesirable from the perspective of the Bank of England. Any further declines in the manufacturing sector could see higher unemployment, highlighting the fact that the global slowdown is now having a significant, direct impact on the UK economy.

Sterling losses would undoubtedly have proved more significant throughout this period were it not for similarly disappointing economic data from Germany, which, whilst remaining the eurozone’s largest and most significant economy, continues to show signs of strain. German factory orders, export figures and industrial production all deteriorating, reflecting the low demand within the eurozone which in turn results in a further decline of investor confidence.

Sterling gains from point B on the graph came as a result of unemployment data which showed UK unemployment is now at its lowest level since 2008, meaning more people are in employment than ever before. Sterling gains, however, were really boosted by positive wage growth data, which the Bank of England previously highlighted as being a primary factor to measure economic progress ahead of any potential interest rate increase.

Sterling benefitted further from far better than expected September retail sales data, which showed an increase of +1.9% against a forecast +0.4%, although this can largely be attributed to a one-off increase as a result of the Rugby World Cup.

Sterling’s push higher against the euro towards the end of the month was a result of comments from European Central Bank (ECB) President, Mario Draghi, who announced that due to poor fundamentals from the eurozone that the ECB will need to assess whether their quantitative easing (QE) programme might need extending. Whilst this was largely expected, the fact that President Draghi then went on to state that they will also consider a host of other policies, including potentially lowering the deposit rate below the current -0.2% level (meaning banks would have to pay more to park money with the ECB) or increasing the level of quantitative easing above what are already significant levels, confirmed the significant trouble the Eurozone finds itself in.

All of the options outlined potentially make the euro a far less attractive investment, with the single currency showing significant losses against most major currencies.

Outlook

Sterling’s ability to continue to strengthen depends on an improvement of the recent disappointing economic data, but more importantly the Bank of England’s Monetary Policy over the coming months.

In the short term recent sterling gains could quickly reverse if the Bank of England was to take the unlikely step of cutting interest rates below the current record low of 0.5%.

Inflation remains a significant concern for the Bank of England. Forecasts earlier this year had highlighted their belief that inflation would have returned to the 2% target level by now. The CPI (Consumer Price Index) inflation reading announced in October, though came in at a very disappointing -0.1% for the second time this year meaning inflation is at the joint lowest reading since 1960.

The UK now faces the very real threat of slipping into deflation with Bank of England forecasts now indicating inflation will only be as high as 1% by next spring. It is worth noting that an interest rate increase remains less likely whilst inflation remains below the target level.

Sterling gains were at risk of evaporating towards the end of October as a result of comments from Bank of England hawk, Ian McCafferty, who has remained the only pro rate rise voter over recent months, but used a speech on October 20th to note that, “Despite the most obvious direction of a rate move being upwards a potential cut in rates could not be ruled out”.

This fact has been exacerbated by recent increases in downside economic risk and the threat of deflation, raising the threat that, whilst unlikely, the Bank of England could consider extending monetary stimulus in the form of adding to their quantitative easing programme. This would almost certainly prove detrimental to the strength of the GBP.

Despite comments from Mario Draghi at the start of October claiming the Eurozone had “returned to sustained growth under the impulse of our monetary policy”, economic confidence remains at extremely depressed levels, not helped by the recent Volkswagen scandal.

With so much uncertainty it seems likely that further stimulus will be required to invigorate economic growth, to the short term detriment of the euro.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Estate Agents Code of Conduct

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.