Sterling/Euro Currency Review October 2014

Tuesday 04 November 2014

Sterling failed last month to add to impressive gains made against the euro in September as the euro continues to demonstrate significant resilience, says Ben Scott.

Despite the European Central Bank (ECB) introducing policies such as Asset-Backed Securities (ABS), many economists feel that without a full blown Quantitative Easing (QE) programme, the economic outlook for the eurozone will remain bleak for some time.

Deteriorating economic fundamentals have lead some commentators to suggest the eurozone, once more, stands on the brink of crisis, yet euro buyers will be concerned by the decrease in economic growth in the UK. This, combined with the mixed messages from the Bank of England (BOE) prevented further Sterling gains last month.

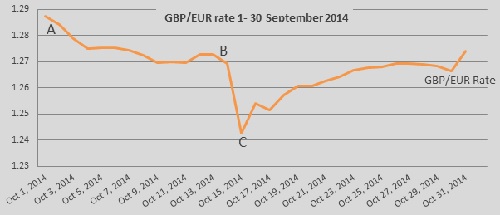

An initial GBP/EUR high of 1.2873 (Interbank throughout) as illustrated by point A on the graph, was followed by a period of uncertainty, including a low of 1.2426 (15 October 2014), trading at an average rate of 1. 2686 throughout October.

Disappointing economic data from the eurozone, particularly Germany - the largest and most important economy in the eurozone - kept the pressure firmly on the ECB to act in an effort to counter the threat of deflation and boost an unacceptably slow economic recovery. The eurozone continues to be hampered by poor industrial production, deteriorating economic sentiment and high levels of unemployment.

Euro gains from point B came despite ECB President Mario Draghi failing to provide any hints on QE, in spite previously stating that they were ready to use "unconventional tools" in a bid to boost ailing economic conditions throughout the eurozone.

The announcement that the ECB plans to embark on a two-year purchase programme of up to €1 trillion’s worth of asset-back securities actually lead to the euro strengthening as expectations were undoubtedly for a larger scale form of QE.

Despite the confused signals from the ECB, Sterling came under pressure early in October as concerns grew that the poor economic performance of the eurozone, which looks set to result in it officially slipping back into recession, would impact UK exports. The UK economic recovery is therefore a concern, validated by the announcement that it had only expanded by 0.7% in Q3 from 0.9% in Q2- 2014. UK Chancellor, George Osborne, added to concerns by stating, “the UK cannot and will not be immune to a (eurozone) slowdown ".

Significant Sterling losses illustrated from point B were a result of the announcement that inflation in the UK fell to a five-year low of just 1.2% from a previous reading of 1.5% in September - well below the Bank of England (BOE) mandate target of 2%.

Falling inflation removed any ongoing pressure on the BOE to raise interest rates in the short-term with many analysts now forecasting the first rate rise in the second half of 2015. Ben Brettell (Senior Economist at Hargreaves Landsdown) stated, "with inflation predicted to fall further in coming months, those hoping for a pre-election interest rate rise are highly likely to be disappointed".

Sterling losses were significant on the back of this disappointing inflation data. However, losses would almost certainly had been deeper were it not for the announcement from the Office of National statistics that the unemployment rate fell to 6%, its lowest level since late 2008.

Positive Sterling gains were quickly re-established from point C, despite unrealistic and somewhat misleading quotes from French Prime Minister, Francois Hollande, that the "eurozone crisis is over". Spain experienced an unsuccessful ten and 15-year bond auction, raising concerns of liquidity problems and stress in the European markets - issues which have weighed heavily on the euro in the past.

Outlook

UK economy growth continues, although at a slightly slower pace than previously seen. Data releases have been falling below forecast since July, raising concerns that Sterling is likely to fall if economic data continues in this adverse trend.

Meanwhile, talk of an interest rate hike from the BOE is firmly on the backburner, and with the UK’s economic recovery remaining unbalanced, in part due to slow wage growth, with little scope of an increase before elections next May. This is likely to prevent any sustainable improvements for Sterling in the short-term.

Euro concerns, as a result of disappointing economic data, looks set to continue in the medium-term. The most pressing issue for the ECB, however, remains falling inflation. With a report at the end of October showing German inflation dropped to -0.3% against a forecast -0.1%, these pressures look unlikely to abate and could force the ECB to introduce a significant quantitative easing programme, which would almost certainly prove detrimental to the euro.

Elsewhere, the International Monetary Fund (IMF) announcement, which cut world growth forecasts from 3.4% to 3.3%, whilst warning that the recovery is "weak and uneven", added further pressure to the eurozone economy which has already been depleted by sanctions imposed on Russia as a result of the Russian/Ukraine conflict. Sanctions, which have directly contributed to German factory orders registering its largest decline since 2009, whilst investor confidence in the eurozone sits at the lowest level since May 2013, will likely to add to euro weakness going forward.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: Diagnostics on Building Surveys

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.