French Income Tax Return 2020 - Unfurnished Rental Income

Thursday 14 May 2020

How to complete your income tax declaration this year if you are a small landlord letting unfurnished property in France.

Unfurnished rental income rental income is taxed under a system of revenus fonciers, meaning, literally, 'real estate income'.

Most of those who let such accommodation (or non-residential property) have the choice of either being taxed on the basis of a fixed cost allowance, called micro-foncier, or on the basis of eligible costs and income, called the régime réel.

In both cases, the social charges, called the prélèvements sociaux also apply, although you can claim exemption (see below).

Those who choose to be taxed using the system of régime réel will normally need to use an accountant to undertake their book-keeping and prepare their income tax return, so we do not propose to go into tax declarations for such landlords in this note.

We say more about this tax system in our comprehensive Guide to Taxation of Unfurnished Lettings.

The vast majority of small landlords in France have no need to use régime réel, as the system of micro-foncier should serve their requirements and it easy to understand and to use.

Eligible landlords are those whose total gross rental income from unfurnished property does not exceed €15,000 a year. If your income exceeds this amount you are required to use the system of régime réel.

Under micro-foncier there is no need to maintain a set of accounts, or to calculate your profit or loss for the purposes of declaring your income.

Only actual cash receipts are considered, so where the rental income has not been paid, or is received late, and beyond the tax year, it is excluded.

You simply record the cash received on the tax return, against which you will be granted a fixed cost allowance of 30%, meaning you will be taxed on 70% of your income.

Accordingly, provided your actual eligible costs are less than 30% of gross income then you would benefit from being taxed under this system. If your costs are higher then you need to consider the system of régime réel.

Your rental income will be added to your other income to arrive at your total taxable income, on which the standard income tax bands and rates will apply.

On-Line Account

In order to declare on-line to make the declaration you will need to connect to Impots.gouv.fr and click on 'Votre Espace Particulier' and create an account with 'Création de mon espace particuliere.'

You will need to obtain from your first tax notice (avis d'imposition) your:

- Numéro fiscal;

- Numéro d'accès en ligne;

- Revenu fiscal de référence.

If you have not previously made a declaration you will need to submit a paper declaration.

Form 2042

The form to use to declare your unfurnished rental income is the main return, F2042. There is no need to use the Form 2044, which you will see referred to on the on-line tax declaration. This form is only for those using the régime réel.

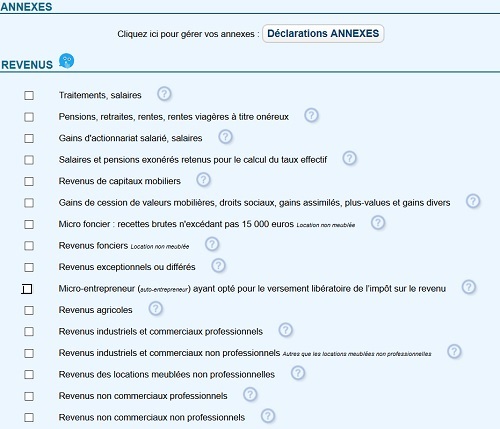

To declare unfurnished rental income on-line, on the F2042, in the 'Étape 3' page titled 'Revenus et Charges' you need to tick the box 'Micro-foncier: recettees brutes n'excedant pas €15,000 - Location non meublé'. You will also need to tick other boxes for other income, although some may already be ticked by the tax authority if you have previously made a tax declaration in France.

The graphic below shows the page and the relevant box. If you are making a paper declaration it does not apply.

You then need to go to page 4 of the form, Section 4 Revenus Fonciers, and enter in Line 4BE the gross rental income figure received in 2019.

If it is foreign rental income (property based outside of France), in addition to entering the details above you also need to state the foreign income in Line 4BK, to ensure you are granted a tax credit for such income. Foreign rental income is not taxable in France, although the income will be added to your France taxable income to determine the rate that applies on that income.

If you have rental income from both France and abroad, then Box 4BK should contain merely the income from abroad.

Below the figure you need to enter the address of the property (or properties) and the name of the tenant(s).

A graphic of the relevant section of the declaration is shown below.

If you let an unfurnished property using a particular type of tax regime such as 'Robien' or Borloo' you cannot benefit from use of the system of micro-foncier. However, similar schemes such as 'Scellier', 'Duflot' 'Pinel' and 'Dormandie' are eligible.

There is similar exclusion for listed buildings (monuments historiques), properties located in conservation areas (Malraux) and urban revitalisation areas (Zone Franche Urbaine).

If the property is held through a French property company (Société Civile Immobilière (SCI) it is still possible to use this tax regime, provided you do not use company taxation. Those in such a 'fiscally transparent' company will be liable for tax on an individual basis in proportion to their own share of the income of the property, and to the extent to which they are otherwise liable to French income tax.

Social Charges

In addition to income tax a landlord is liable for the social charges, called the prélèvements sociaux, at the rate of 17.2% on net rental income, ie 70% of the gross income for those using the system of micro-foncier. This charge is deductible against income tax at the rate of 6.8%.

Non-residents from outside of the EEA are also liable for the social charges of 17.2% on unfurnished lettings, although EEA residents not formally in the French health system (S1 holders) only pay a 'solidarity tax' at the rate of 7.5%.

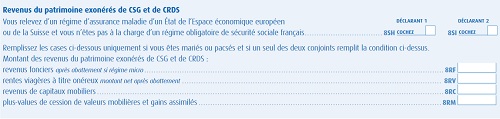

If you are exempt from social charges as you are not affiliated to the French health system (S1 holders or non-resident), then on-line you need to go the page on F2042, headed 'Divers' and the section 'Revenus du patrimoine exonérés de CSG et de CRDS' and tick one or both Boxes 8SH and 8SI, depending on your circumstances.

You then need to enter the income received, after deducting the allowance of 30%, in the Box 8RF.

If you have not previously made a tax declaration in France then your (personalised) on-line F2042 may not include these boxes, so you need to use Form 2042C (Déclaration Complementaire), to claim exemption from social charges. This form is used mainly to declare certain types of investment income, but it includes on it the above section, using the same headings and box numbers.

The graphic below shows the relevant section on the page.

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.