PUMA Health Charge Exemption Doubled

Wednesday 07 November 2018

The government have revealed details of the changes that are to be made to the PUMA state health insurance charge.

As we reported last month, the health charge has been the subject of legal controversy, culminating in a hearing in the Constitutional Council, which resulted in a let-off for the government on the promise of reform.

The charge is levied on those with little or no income from

salaried employment or business, but who earn investment income from

rents, savings and capital gains. It is only applied on investment

income, but those in receipt of a pension are entirely exempt.

At the end of September the government issued a statement of their intent, which they have since now set out in more detail in the social security finance bill for 2019.

In their explanatory statement introducing the draft bill they admit to «certaines incohérences» and «des défauts de conception de la contribution», a surprising admission of guilt, but one forced on them by the legal ruling.

The extent of the changes now proposed are substantial, and it is likely to mean that most households who are 'economically inactive' will obtain free affiliation to the French health system.

There are three main changes:

- The investment income threshold limit that grants exemption will be increased from €9,654 per person to €19,866 (2018);

- The percentage rate payable will be reduced, from 8% down to 6.5%;

- The minimum income threshold that makes those with a professional activity liable increases from €4,000 to €8,000.

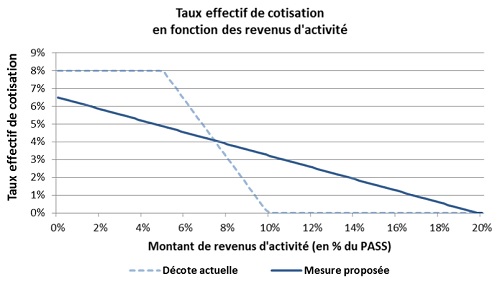

Broadly speaking, therefore, those who are liable will pay 6.5% on investment income over €20,000, although for those with a professional activity AND investment income the rate is tapered.

Currently, those with a professional activity are exempt from the charge if their professional income is greater than €4,000 pa, due to the social security contributions they pay on such income. The government decided that the limit was too low.

In future, the minimum professional income limit to will increase to €8,000 per annum, but with the charge rate reducing progressively with an increase in professional income, as follows:

The change means that only those with a professional activity earning below €8,000 pa, and capital income greater than €19,866, would be liable for the charge. In the case of a married couple or those in a civil partnership, the charge will not apply to either of them where one of them has income from a professional activity above the threshold.

This same rule applies in relation to those couples where at least one of them is in receipt of a pension, when they are both them exempt from the charge.

An upper limit to the capital income that gives rise to the charge is also being introduced, equivalent to €317,000 (2018). So income over this amount will be exempt from the charge, a change that will benefit around 500 individuals.

Exceptional capital gains remain liable.

The changes will be effective from 2019, but as the charge is levied in arrears it will be billed at the end of November 2020.

Early Retirement Pensions

There is no further clarity given to the status of those on early retirement pensions.

In this context the legislation makes no distinction between State retirement early retirement pensions, or between French pensions

and international pensions. Making a distinction between the latter would, in any event, be problematic on constitutional grounds.

All of which means, in law at least, those in receipt of any pension or annuity are not liable for the charge.

The evidence on the ground is a mixed one, but it does seem from your mails that the overwhelming majority of expatriate early retirees are being exempted or liable for only a small charge.

The PUMA charge is affecting few households, and with the changes that have been announced it will affect even fewer next year.

Whether is was the original intention of lawmakers to grant such wide exemption is not clear. Alternatively, it may simply be that a right to affiliation without charge is being

granted by virtue of social charges payable on pension income. We can only speculate on that point.

In addition, there continues to remain legal uncertainty about the right of early retirees from the EEA with less than 5 years legal residence to obtain affiliation to the French health system, an issue we consider in our guide to Health Insurance in France for Early Retirees.

Private Health Insurance

Similarly, the draft proposals are silent on the liability of those with private health insurance; many of you with private policies and, therefore, outside of the State system, have been obliged to pay the charge this year.

It seems, at least as far as the social security agencies are concerned, that having a private policy, by its own, does not grant exemption from the charge, with URSSAF the social security collections agency stating to us earlier this year: "La souscription d’une assurance privée est sans conséquence à ce titre sur l’assujettissement à la cotisation."

This leaves the status and future of private health cover in France in some uncertainty. From appeal decisions of which we are aware, only those with a private policy AND in receipt of a pension are being exempted.

There is no intention in the new law to retroactively correct the three years of “incohérences", as a result of which Eric Fenster, a member of AARO (Association of Americans Resident Overseas) fighting a battle for many US citizens with private health policies comments that: "This means the challenges to the CSM charges for 2016, 2017 and 2018 must still be maintained."

"For Americans, universal health coverage realizes a dream, but people weren't informed that they were considered to automatically benefit from cover despite not being enrolled. The prefectures wrongly kept forcing them to prove subscriptions to private policies; then they received the first CSM bill after nearly two years of phantom, unusable 'coverage' ", he stated.

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.