French Income Tax Return 2019 for Rental Income

Tuesday 07 May 2019

How to complete your income tax declaration this year if you let out furnished property in France.

POSTSCRIPT: We have published a guidance note on the process for the 2020 tax return at French Income Tax Return 2020 - Furnished Rental Income, so the following page has been superceded.

There is also a guidance note on French Tax Return 2020 - Unfurnished Rental Income.

The income tax declaration for those who let furnished property has been complicated this year by the introduction of deduction at source, a change which we reviewed in our article Taxation of Income in 2019.

Unless you complete the form correctly you will not benefit from the tax credit that should otherwise exempt most landlords from income tax and social charges on their 2018 rental income due to the introduction of deduction at source.

The form to use in declaring your rental income is a supplementary form to the main 2042, called 2042-Pro.

However, for the purposes of the guidance given below you also need to indicate on Form 2042 in 'Etape 3', that you will be declaring furnished rental income. If you are making the return on-line, this will ensure the relevant form and sections open out to you for completion.

Furnished Lettings

The definition of 'furnished lettings' (locations meublées) for the purpose of the tax declaration are those residential properties that are let out on either a short-term or long-term basis, whether a house, apartment or chambre d'hôte.

Those who let out furnished lettings may be:

- Professional or non-professional landlords;

- Business registered or not business registered;

- Resident or non-resident.

- Régime Réel

- Micro-BIC

- Micro-Fiscal

Those who adopt the régime réel apply accounting rules to the determination of their income, and they are liable for tax on their net income after deduction of eligible costs. Such landlords are likely to use an accountant for their accounts and submission of their tax declaration, so we will not be considering them in these notes.

Similarly, those are landlords of investment properties let out under special tax regimes, and those who let unfurnished property, are not covered in this guidance.

For a fuller explanation of these rules, you can read our Guide to Letting Property in France.

i. Micro-BIC

If you have adopted the micro-bic tax status you will be assessed for income tax and social charges on your gross annual rental income, less a fixed cost allowance – either 50% or 71%, depending on the nature of the accommodation.

Properties that benefit from the higher allowance are accredited meublés de tourisme classés and all chambres d'hôtes.

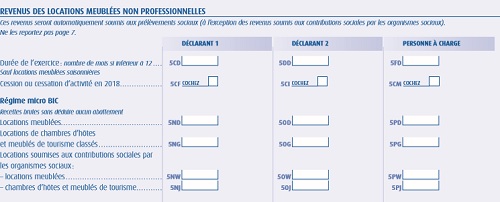

You will need to track to the section headed 'Revenus des Locations Meublées Non Professionnelles', where you should enter your gross rental income in either box 5ND or 5NG, depending on the type of your letting.

ii. Micro-Fiscal

Those businesses registered as a micro-entrepreneur can opt to pay a flat-rate income tax with their similarly flat-rate social security contribution, under a system called micro-fiscal. So if you are not a registered micro-entrepreneur this section does not apply to you.

It is not ordinarily advantageous to be taxed in this manner, unless you have substantial other earnings. There are also limits on its use if your income is above a certain threshold.

In addition, you will not be entitled to a tax credit for 2018, so the section of this note on the tax credit does not apply to you. You can read more in our Guide to Microentrepreneur Business in France.

If you have opted for micro-fiscal, you should go to the opening page of the Form 2042-Pro where it is headed 'Micro-Entrepreneur (auto-entrepreneur) ayant opte pour le versement de liberatoire de l'impot'.

You need to enter your gross income in box 5TB : 'Prestations de services et locations meublées'.

Tax Credit

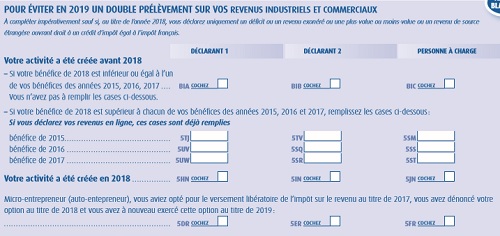

For those who use Micro-BIC, in order to benefit from the tax credit you first need to go to the section headed 'Pour Eviter en 2019 un Double Prélévement sur vos Revenus Industriels ou Commerciaux'.

- If your turnover in 2018 was not greater than the three years average of 2015-2017, then tick box BIA; if greater, leave blank;

- If your turnover in 2018 was greater than your previous three-year average then declare the turnover for each year in boxes 5TJ, 5UV, and 5UW, as necessary;

- If you only started the business in 2018 then tick only box 5HN.

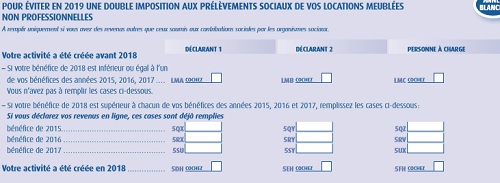

In addition, you also need to go to the section below headed 'Pour Éviter en 2019 une Double Imposition aux Prélévements Sociaux de vos Locations Meublées Non Professionelle'.

- If your turnover in 2018 was not greater than the three years average of 2015-2017, then tick box LMA; if greater, leave blank;

- If your turnover in 2018 was greater than your previous three-year average then declare the turnover for each year in boxes 5QX, 5RX, and 5SU, as necessary;

- If you only started the business in 2018 then tick only box 5DH.

The above advice is given on a general basis only; you need to seek professional advice on your individual cirumstances. See our article French Income Tax Return 2019 on the various forms.

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.