French Income Tax Return 2020 - Furnished Rental Income

Thursday 14 May 2020

How to complete your French income tax declaration this year if you are a small landlord letting out furnished property in France.

Furnished Lettings

The definition of 'furnished lettings' (locations meublées) for the purpose of the tax declaration are those residential properties that are let out on either a short-term or long-term basis, whether a house, apartment or chambre d'hôte. It also includes stationary mobile homes.

Those who let out furnished lettings may be:

- 'Professional' or 'non-professional' landlords;

- Business registered or not business registered;

- Resident or non-resident.

Depending on your circumstances and the choices you make, the method of taxation of the rental income you receive may be either:

- Régime Réel;

- Micro-BIC;

- Micro-Fiscal (micro-entrepreneurs only)

Those who adopt the régime réel use accounting rules for the determination of their income, making them liable for tax on their net income after deduction of eligible costs. You will need an accountant for your accounts and submission of your tax declaration, so we do not consider such landlords in these notes. For a fuller explanation of the rules relating to the régime réel you can read our Guide to Letting Property in France.

Similarly, those who are landlords of investment properties let out under special tax regimes (Scellier, Robien etc) are not covered in this guidance.

On-Line Account

In order to declare on-line to make the declaration you will need to connect to Impots.gouv.fr and click on 'Votre Espace Particulier' and create an account with 'Création de mon espace particuliere.'

You will need to obtain from your first tax notice (avis d'imposition) your:

- Numéro fiscal;

- Numéro d'accès en ligne;

- Revenu fiscal de référence.

If you have not previously made a declaration you will need to submit a paper declaration to your local tax office. Forms are available for downloading on-line.

Forms

The form to use to declare your furnished rental income is a supplementary form to the main F2042, called F2042-C-Pro, although both forms will need to be submitted.

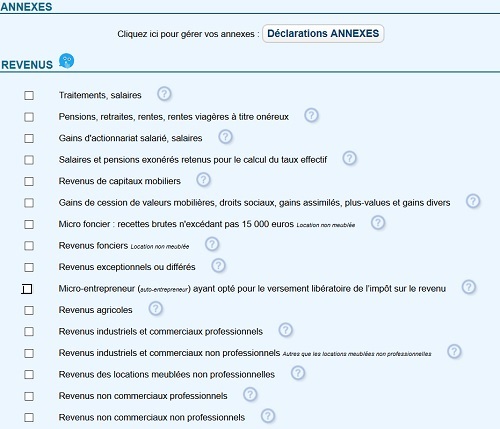

Before you can start to enter your income on 'Pro' you need to indicate on F2042 that you will be declaring furnished rental income. If you are making the return on-line, this will ensure the relevant form and sections open out to you for completion.

To declare furnished rental income, on the F2042, in the 'Étape 3' page titled 'Revenus et Charges' you need to tick the box ''Revenus des locations meublées non professionnelle'.

Alternatively, if you are pursuing the activity as a registered micro-entrepreneur, who has opted to pay income tax under the system of 'micro-fiscal', you need to tick 'Micro-entrepreneur (auto-entrepreneur) ayant opté pour le versement libératoire de l’impôt sur le revenu '. If you have any doubts about what this means, refer to our guide below.

The graphic below shows the page and the relevant boxes.

If you let furnished property in France through Airbnb, Abritel, Booking.com or similar websites, you should have received from the operator details of the income received, which, under new rules this year, they will also have communicated to the tax authority.

i. Micro-BIC

If you have the standard micro-bic tax status you will be assessed for income tax and social charges on your gross annual rental income, less a fixed cost allowance – either 50% or 71%, depending on the nature of the accommodation.

Properties that benefit from the higher allowance are meublés de tourisme classés and all chambres d'hôtes.

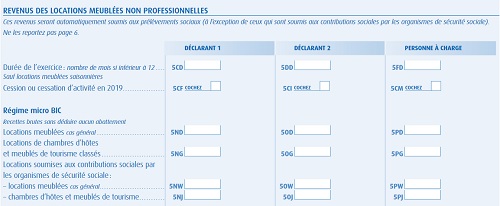

On the F2042-C-Pro you will need to track to the section headed 'Revenus des Locations Meublées Non Professionnelles'.

If you are not a micro-entrepreneur landlord, you should enter your gross rental income in either Boxes 5ND/50D for general furnished lettings or Boxes 5NG/5OG for chambres d’hôtes and meublés de tourisme classés.

A couple can divide total income between them and insert each share of the income in the relevant boxes (Déclarant 1/2), but really only important if their liability to social charges is not the same as the total income is divided in the tax assessment.

If you are a micro-entrepreneur landlord, you should enter your gross rental income in either Boxes 5NW/5OW or Boxes 5NJ/OJ as appropriate, EXCEPT those who have elected for 'micro-fiscal' (see below). This is to ensure that you do not pay social charges on your rental income, as you pay social insurance contributions each month/quarter. A couple should only divide the income (Déclarant 1/2) where they are both business registered.

If it is a seasonal letting activity you have no need to complete the line 'Durée de l’exercice'.

ii. Micro-Fiscal

Those businesses registered as a micro-entrepreneur can opt to pay a flat-rate income tax with their similarly flat-rate social security contribution, under a system called micro-fiscal. So if you are not a registered micro-entrepreneur this section does not apply to you.

It is not ordinarily advantageous to be taxed in this manner (although that may not always be the case for non-residents) unless you have substantial other earnings. There are also limits on its use if your income is above a certain threshold.

If you have opted for micro-fiscal, you should go to the opening page of the Form 2042-C-Pro where it is headed 'Micro-Entrepreneur (auto-entrepreneur) ayant opte pour le versement de liberatoire de l'impot'.

You need to enter your gross income in Boxes 5TB/5UB as appropriate : 'Prestations de services et locations meublées'. That is all you need do.

Social Charges

Those who are not affiliated to the French health system (S1 holders or non-resident) are exempt from social charges on their rental income.

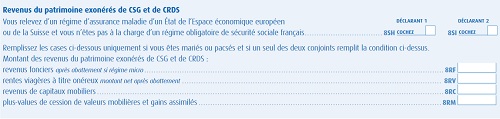

In order to obtain this exemption (and only if you are not a micro-entrepreneur landlord), you need to use Form 2042C (Déclaration Complementaire) and head to Section 8, 'Divers' and the part 'Revenus du patrimoine exonérés de CSG et de CRDS'. You should tick one or both Boxes 8SH and 8SI, depending on your circumstances.

If you have previously made a tax declaration in France, this section may be included in your (personalised) on-line page on the main F2042, in which case there will be no need to use a separate form.

If you have not previously made a tax declaration in France, and/or you are making a paper declaration, then your paper F2042 will not include these boxes, so you need to use it to claim exemption from social charges.

The Form 2042C is used mainly to declare certain types of investment income, but it includes on it the above section, using the same headings and box numbers.

That should ensure that social charges are not be imposed on your rental (or other capital) income, although you will be liable for the solidarity tax (prélèvement de solidarité) at the rate of 7.5%.

Where only one member of the household is exempt, there is no provision on this section to state the amount of income that should be exempt, but the French tax office advise that in the case of furnished rental income it will happen automatically.

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.