French Income Tax Return 2020 - Micro-Entrepreneurs

Thursday 14 May 2020

How to declare your business earnings for 2019 on your 2020 income tax declaration if you run a micro-entreprise business in France.

As part of their annual income tax declaration micro-entrepreneurs need to complete Form 2042-C-Pro (Déclaration Complémentaire), an annex to the main Form 2042.

Completion of the form depends on the method of taxation you have chosen and the nature of your business activity, as we show below.

The declaration is made on-line, unless you are making a declaration for the first time, when you complete a paper declaration.

We do not consider in this note those who let out furnished property as a registered micro-entrepreneur, which is considered separately in our article Taxation of Furnished Rental Income.

On-Line Account

To make the declaration on-line you will need to connect to Impots.gouv.fr and click on 'Votre Espace Particulier' and create an account with 'Création de mon espace particuliere.'

You will need to obtain from your first tax notice (avis d'imposition) your:

- Numéro fiscal;

- Numéro d'accès en ligne;

- Revenu fiscal de référence.

If you have not previously made a declaration you will need to submit a paper declaration.

Form 2042

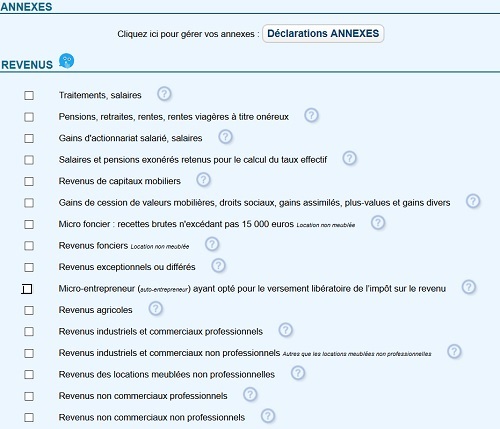

To declare business income on-line, on the F2042, in the 'Étape 3' page titled 'Revenus et Charges' you need to tick a relevant box on the main page headed 'Selectionnez ci-dessous les rubriques que vous souhaitez faire apparaitre'.

If you have not elected to pay flat-rate income tax each month with your social security contributions then you tick either the box 'Revenus industriels et commerciaux professionnels' or 'Revenus non commerciaux professionnels', depending on your business category (or both if you have both types of income).

Alternatively, if you have opted to pay income tax under the system of 'micro-fiscal' you need to tick 'Micro-entrepreneur (auto-entrepreneur) ayant opté pour le versement libératoire de l’impôt sur le revenu '.

The graphic below shows the page and the relevant box. If you are making a paper declaration it does not apply.

The two methods of taxation are Régime de Base and Micro-Fiscal.

i. Régime de Base

The default method for assessment is using the standard tax rates, on the information you provide in your income tax declaration, including your other income and household circumstances.

Under this option, a standard cost allowance against turnover is granted, the level of which depends on your business category – either 71%, 50% or 34%.

Clearly, this is the preferred option if you pay little or no income tax.

You simply declare your turnover (cash received) for the year.

If you are unsure of your turnover, then (normally) you are able to go to your URSSAF on-line account, 'Mes Documents/Mes Attestations', and download your 'attestation fiscale', which provides the information you need to assist you with your income tax declaration. This year, due to Covid-19, this declaration may not be available.

For trade, commercial and service based activities the relevant section of the Form 2042-Pro headed ‘Revenus Industriels et Commerciaux Professionnels'.

The relevant boxes are:

- 5KO : commercial activities (BIC);

- 5KP : trade and service based activities (BIC);

For those who are a profession libérale on the same form is the section headed ‘Revenus Non Commerciaux Professionnels'

The relevant box is:

- 5HQ : liberal professions (BNC).

ii. Micro- Fiscal

Alternatively, a micro-entrepreneur has the option to pay a flat-rate monthly/quarterly percentage figure of their turnover, which they pay alongside their similarly flat-rate social security contribution. With this option no cost allowance is granted.

The option for periodic payment of income tax is called micro-fiscal, but is also called the prélèvement libératoire.

The rates of income tax for micro-fiscal vary by nature of business activity :

- 1% for commercial sales;

- 1,7 % for trade and service based activities ;

- 2,2 % for the professions libérales who are BNC.

In terms of the income tax declaration the section to complete is 'Micro-Entrepreneur (auto-entrepreneur) ayant opte pour le versement de liberatoire de l'impot', which is located at the beginning of Form 2042-Pro.

You need to select the relevant boxes, depending on your business category:

- 5TA : for commercial activities (BIC);

- 5TB : for trade and services based activities (BIC);

- 5TE : for liberal professions (BNC).

In the relevant box you declare your turnover (cash received).

If you are unsure which tax system you are using, when you make the on-line declaration of your turnover, the declaration form will indicate at the top if you have opted for the prélèvement libératoire.

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.